Searching for value

To hear it told, the hand that placed the last piece of the puzzle completed the picture.

The Carnegie Corporation of New York accepted Eagle Grove’s application of a grant for $10,000 to build a library building on April 26, 1902. The library was designed by the Des Moines architect firm Smith and Gage in the Beux Arts style. Dedicated on September 15, 1903. It is a brick structure with a conical-roofed entrance pavilion with four engaged columns in the logic flanking the main entryway. The public library has subsequently moved to a larger facility during 1976 and the old library building was turned over to the Local Historical Society as a museum. The building was listed on the National Register of Historic Places in 1983.

Eagle Grove is a town of 3600 located in deep agriculture country in central Iowa.

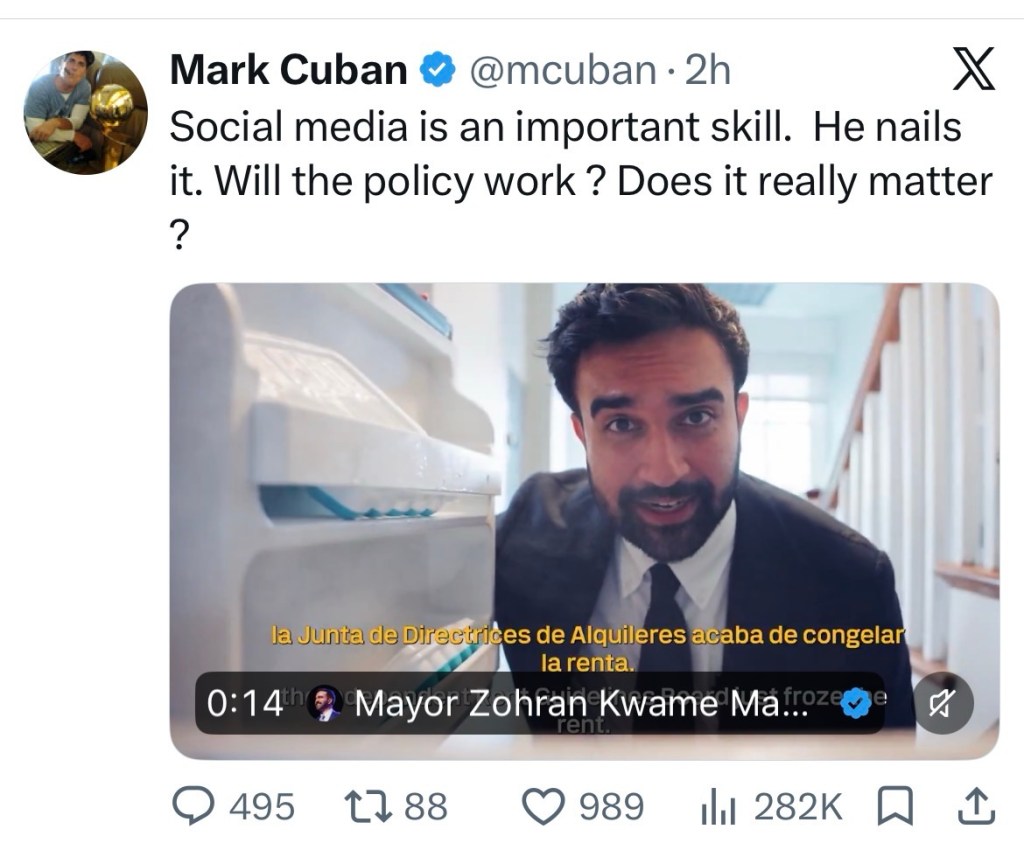

“Renters’ rights” has become a rallying cry among a growing class of people who have appointed themselves advocates for the renter community. It is worth noticing what that means. Many of these advocates neither own the properties in question nor rent them. They do not maintain the units, pay the mortgages, make the repair decisions, or bear the consequences when those decisions turn out to be wrong. They are observers, giving political voice to their interpretation of a relationship between two parties who are actually making the decisions.

So let’s start at the level where the rental market works reasonably well for, say, 90 percent of landlords and tenants.

There is no such thing as “the rental property” or “the renter.” There are properties in varying conditions, in different locations, with different amenities and different levels of maintenance. There are tenants with different incomes, preferences, standards, and expectations. And there are landlords ranging from meticulous owner-occupants to large property managers. Some are excellent. Some are indifferent. Some are terrible.

That is precisely what we should expect in a voluntary market.

A landlord offers a particular product at a particular price. A tenant decides whether that product is worth the price. If it isn’t, the tenant can leave. Maybe they move next door. Maybe they move across town. Maybe they find a better unit for the same rent.

That ability to leave is not a trivial feature of the arrangement. It is one of the mechanisms through which the market disciplines both sides.

Landlords, meanwhile, have an obvious reason to keep good tenants. They have an equally obvious reason to maintain the property. Maintenance preserves the capital they own. A neglected property loses value. Poor maintenance drives away good tenants. Deferred repairs become more expensive repairs. Eventually, the owner pays for the neglect through lower rents, higher turnover, larger repair bills, or a lower sale price.

This is ownership.

Yet you would rarely know it from much of the renter-rights conversation. The landlord is routinely cast as a wealthy, absentee, quasi-parasitic figure who owns an inexhaustible supply of appreciating property and needs to be forced to spend money on it. What gets left out is the rather important fact that buying, financing, maintaining, and eventually selling property can produce losses. The owner takes the capital risk. The tenant does not.

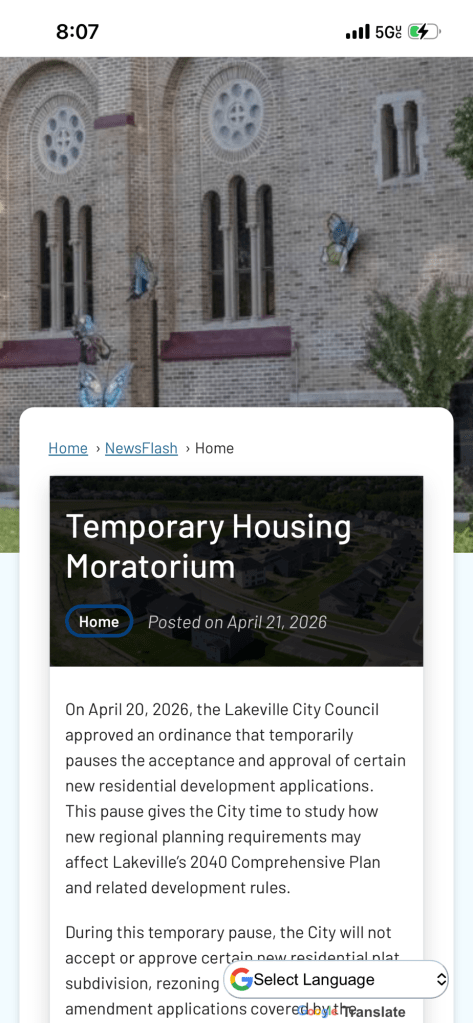

Now we have a new proposal for inserting renters into the ownership relationship: the “Right to Repair.”

Thankfully, this week the St. Paul City Council denied the request for Right to Repair to appear on the ballots this fall:

Citing a critical last-minute memo from the city attorney’s office, the St. Paul City Council voted Wednesday to block a proposed “Right to Repair” tenants’ rights ordinance from proceeding to the November ballot. Organizers, who spent Thursday morning meeting with attorneys, said they are reviewing their legal options.

The ballot question, proposed by the Safe Homes St. Paul campaign, would have asked voters to approve a new city ordinance that would allow residential tenants to devote up to $500, or half their rent, whichever is greater, toward completing their own home repairs.

The problem is not that repairs are unimportant. Of course they are.

The problem is who gets to decide what constitutes a repair, what the repair should be, who should perform it, and who should pay for it.

There are legitimate circumstances in which one property owner’s decisions affect others. A sewer system is a good example. It functions because everyone connected to it is constrained from dumping solvents or other toxins into the system. Some aspects of property necessarily involve obligations to other property owners.

But imagine extending this logic.

Suppose my neighbor has an ugly driveway full of weeds and cracked pavement. I believe it is an eyesore. I also believe it is hurting my home’s resale value. Why shouldn’t I invoke my “right to repair,” have the driveway fixed, and send my neighbor the bill?

Obviously, that wouldn’t be neighborly.

Yet the principle becomes considerably less absurd only because we have decided that the person who owns the property should generally retain the authority to decide what happens to it.

Some parts of housing are shared. Many are not.

And that distinction matters.

Tenant-rights advocates may sincerely believe they are improving the housing stock through political organizing. But there is a fundamental mistake in confusing an interest in a property with an ownership interest in that property.

A tenant has an interest in having a decent place to live. That does not give the tenant an ownership claim over the decisions involved in maintaining someone else’s capital.

If the tenant is dissatisfied with the property, the market already provides an answer.

If the tenant cannot afford to leave, then there is a legitimate policy question about whether that person should receive assistance. Subsidize the person who needs help. Don’t confiscate the decision-making authority of the person who owns the property.

That distinction is crucial.

The alternative is essentially this: I don’t have enough money to move, so I should have the power to make you spend money on your property according to my judgment.

That is not a renters’ right. It is a transfer of ownership authority without a transfer of ownership responsibility.

And that is where the “Right to Repair” becomes something more than a maintenance policy. It becomes a power struggle over who gets to control property.

The socialist instinct is often to separate ownership from control—to leave the title with one person while progressively transferring the decisions to everyone else. But this creates a problem that is often ignored: if you separate responsibility from authority, you weaken the incentive to preserve the asset.

The owner pays for the roof. The owner pays for the furnace. The owner absorbs the loss when the property deteriorates. The owner ultimately bears the consequences of bad capital decisions.

So why should someone who bears none of those costs have the authority to make those decisions?

Ownership is not simply a right to collect rent. It is a bundle of risks, responsibilities, costs, and decision-making authority.

Take away the authority while leaving the responsibility, and you haven’t made the system more just. You have simply made ownership less meaningful.

And when ownership becomes less meaningful, don’t be surprised when people become less interested in owning, maintaining, and improving the property in the first place.

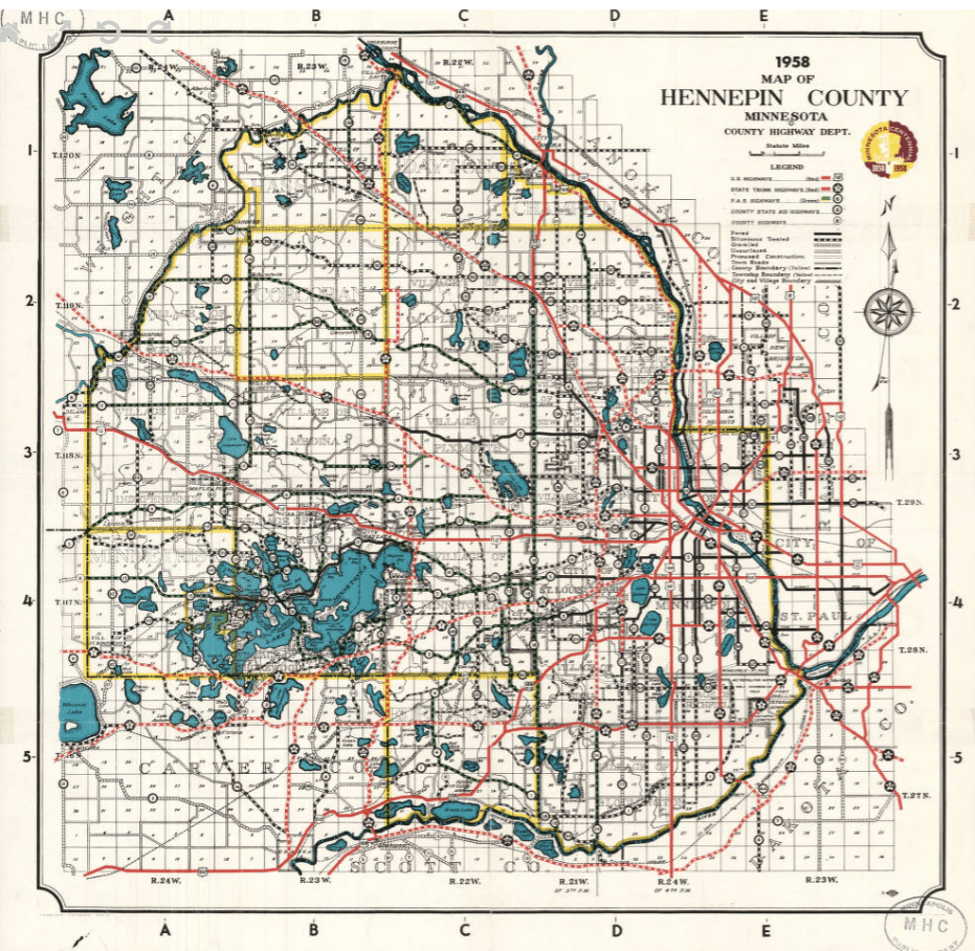

This cool interactive map of Hennepin county shows the networks of roads set out by 1958.

Every red line is a route organized and maintained by the Feds.

The Federal-Aid Highway Act of 1956, also known as the National Interstate and Defense Highways Act, Pub. L. 84–627 was enacted on June 29, 1956, when President Dwight D. Eisenhower signed the bill into law. With an original authorization of $25 billion (equivalent to $220 billion in 2025)[1] for the construction of 41,000 miles (66,000 km) of the Interstate Highway System over a 10-year period, it was the largest public works project in American history through that time.[2] (wiki)

Is it just me or has anyone else noticed the spill over in positive externalities when people pursue something they love?

Corn dominates rail grain volume. Union Pacific is a major Midwest player in this traffic, alongside BNSF and others. Rail’s advantages are cost and capacity over distance, plus lower emissions per ton-mile than trucks—critical when production is concentrated in the Plains and demand is scattered or overseas.

This is a classic grain terminal scene: large cylindrical elevators (silos) with headhouses, leg conveyors, and loading infrastructure feeding a long string of covered hoppers. The cars are the standard dry-bulk type used for corn, soybeans, wheat, etc. UP markings and “Building America” slogan are clear; the CMO car is another common reporting mark in the mix. Graffiti is routine on freight equipment. Power lines, weeds, and the roadside vantage point give it that everyday rural industrial feel under flat Midwestern skies. These facilities are the nodes where local harvest volume concentrates for efficient rail outbound.

Rail is a backbone for moving U.S. crops, especially longer-haul grain. Roughly 24–26% of total U.S. grain (corn, soybeans, wheat, etc.) moves by rail in recent years, with trucks handling the majority (~60–62%, mostly shorter hauls from farm to elevator).

Local courthouses in county seats across the country stand as reassuring symbols of property documentation and the enforcement of law. These imposing buildings often anchor towns with populations as small as 2,700.

This, the third and present courthouse, was built for about $50,000 and completed in 1893. Three stories high except for the clock tower, which rises well above the multi-gabled roof, it underwent extensive renovation in 1974.

If I had to divvy up how I think of actions in housing into three, how would that go?

The first leg is the actions of the people who live in the homes—what they like for their comfort or their physical needs. Their actions in the care and maintenance of the home. It might be their actions in demanding that builders create for them, like whether a granny suite in the lower level is thought into the plan.

The second leg of the stool would entail actions on the physical structures. And yes, there’s overlap here with leg number one. But much more as the structure must bend to the demands of the infrastructure hooking the building into services—electricity, natural gas lines, and water mains. The building must stand up to the expectations of insurance companies and building codes. And the homes must not trouble the earth by being too close to natural habitats or in the paths of wildfires.

The last leg of the stool are the actions taken by all the group work mulling around in the vicinity of the property. Actions taken to support the school district or prevent massage parlors. Actions that plan for shopping malls and means of getting to the airport. The third section that impacts housing are all the formal and informally organized groups offering services to the people in the homes.

Those are my three legs to the housing stool.

Spy/Master is a solid Cold War thriller.

It delivers some classic types done well: the optimistic American CIA agent Frank Jackson, the coolly controlled spy Victor Godeanu, and the erratic dictator Nicolae Ceaușescu paired with his equally driven, obsessive wife.

Filming in Romania itself is a genuine bonus—locations this rarely seen on screen give the series an extra edge.

Like trains of cars on tracks of plush

I hear the level bee:

A jar across the flowers goes,

Their velvet masonry

Withstands until the sweet assault

Their chivalry consumes,

While he, victorious, tilts away

To vanquish other blooms.

His feet are shod with gauze,

His helmet is of gold;

His breast, a single onyx

With chrysoprase, inlaid.

His labor is a chant,

His idleness a tune;

Oh, for a bee’s experience

Of clovers and of noon!

And of course, as I wrote on July 6, while the American housing market is extremely capitalistic in the sense that the key decision-makers are profit-seeking investors, it is very much not a free market. If you own a parcel of land and would like to build a mid-rise apartment on it, the odds are very high that this is illegal. And it will continue to be illegal no matter how many bona fide safety or environmental externality rules you comply with. It’s just normally the case in the United States that you cannot build a four-story, eight-unit building on a plot of land that you own and then rent it out to willing customers.

The above excerpt is from Matt Yglesias’s newsletter today. It reflects perfectly how most public intellectuals define the “housing market.” They treat houses as widgets that are manufactured and sold. In their telling, developers are the primary producers, the main influencers, and the principal profit-takers. Different product “flavors”—most notably “affordable housing”—are then imagined as responses to market prices, even though this notion itself contradicts the idea of freely floating prices.

What they are actually describing is a relatively small slice of the activity that houses people and their families—perhaps 13–15 percent of the relevant transactions. The other 85 percent of household-related exchanges do not involve the new-structure market they fixate on. Because these commentators are widely regarded as authoritative, their narrow and distorted framing circulates as if it were a comprehensive understanding of the housing market.

The reality is that 85–90 percent of the housing market consists of ordinary home buyers and sellers. There is no greedy developer to vilify. Each side of the transaction is simply weighing its own interests—timing, finances, life stage, and personal priorities—when deciding what to offer or accept. People at different points in life bring different advantages and constraints, but the exchange remains primarily between private individuals, not between households and some distant mega-corporation. Corporate or institutional buyers account for only about 6 percent of total sales.

A housing market is the aggregate of these countless private interactions. The prices that emerge reflect what large numbers of people value or dislike about the physical structures themselves, the quality of municipal services, the schools that educate children, the transportation infrastructure, and a host of other local conditions.

So let’s keep the conversation more nuanced and richer in detail. Let’s stop fixating on the small minority of developers who either make a profit or lose their shirts. If we want to talk seriously about housing, we should start by talking about ourselves.

Ice cream is one of the few things that still works exactly as advertised.

No app. No subscription. No “optimized experience.” Just cold, sweet, slightly messy proof that summer still exists.

In Minnesota we don’t take it for granted. We wait all year for the stretch of days when the only decision that matters is soft-serve or scoop, and whether you’re eating it before it melts or racing the melt itself.

Some people treat ice cream like a reward. My go to reward is McDonald’s soft serve. I can find a small treat on a wafer cone as close as the next franchise drive-up.

Sometimes what you need is a destination ice cream, a shop located walking distance from the restaurant you just ate at. Not ready to let go of the company or conversation, off you go to a place like Bebe Zito ice cream. Located across from the Wedge Coop at 22nd an Lyndale, it offered a delicious treat and enabled an already enjoyable evening to be extended a bit longer.

Lakewood Cemetery has been the final resting place for a century and a half of Minnesotans whose names still carry weight—Hubert Humphrey, Paul Wellstone—and for many others whose histories remain quieter, known mainly to the families who return.

The markers meander across gently rolling ground on the east side of an iconic city lake. From one slope you can watch cyclists, walkers, and rollerbladers of every age circle the sky-blue water below.

I was there today for a service held in the chapel just inside the entrance gates. Tile covers the walls and ceiling in a splendid array of images and colors. Seated under the dome, as if gathered inside an apse, the space is neither too large to lose intimacy nor too small to hold a dignified gathering.

The family spoke poetry and psalms. They spoke of family history and of the deeds their loved one had performed in life. They spoke of love, endurance, support, and caring. They reinforced their faith in the belief that they would all be reunited once again.

In death there is renewal.

“To live together in the world means essentially that a world of things is between those who have it in common, as a table is located between those who sit around it; the world, like every in-between, relates and separates men at the same time.“

The last quote is from Hannah Arendt, The Human Condition, Chapter 2 (“The Public and the Private Realm”), specifically the section titled “The Public Realm: The Common.”

I assert here at home economics that there is a private and public side to every transaction; that the course through which the action travels varies if it is primarily tapping private concerns or public concerns.

In this vignette, Professor List asks his audience for their reaction to whether he should pay a student to review his work. The underlying question is whether the student ought to donate his time or treat the request as a paid position—List proposes $50 an hour. The answers that follow are revealing: they disclose the kind of relationship people assume exists between professor and student.

The student is no longer enrolled in the professor’s class, yet one can reasonably infer they still occupy a mentor–mentee relationship. The mentor’s role is to educate and guide. The mentee’s corresponding duty is not to waste the mentor’s time and to make good use of the guidance offered. In this framing the flow of value is unidirectional: a gift of a private good to a private recipient.

An alternative reading treats them as equal members of the college. As participants in the same intellectual community they both benefit by reviewing each other’s work; the knowledge that results is a kind of public good produced by reciprocal sharing. No money changes hands, and the intellectual capital remains with both parties.

A third possibility is the one the student himself seems to have inferred: that the request is private and transactional. Once the exchange is framed that way, the student may collect his fee and then find himself quietly excluded from future opportunities for genuine intellectual exchange. Silent exclusion can be the most costly outcome of all.

But to answer John List’s question one must first set up the problem and identify the groups.

The 2020s have brought a boom of roundabouts across Minnesota’s cities and greater metropolitan area. The Minnesota Department of Transportation reports more than 530 on roads statewide, noting that they “have become an increasingly popular intersection type by traffic engineers.”

It’s common to experience a bit of the “No, you go first” effect as unfamiliar drivers hesitate before entering the circle. Before long, a backup forms on one of the approaches while people figure out the new system.

The reason given for the widespread adoption is safety. MnDOT cites an 86 percent decrease in fatal crashes, an 83 percent decrease in life-altering injury crashes, and a 42 percent overall decrease in the injury crash rate at intersections converted to roundabouts.

They have changed the driving landscape—and provided some comedy relief in the process.

Top reasons for staying or returning;

to care for seniors

to raise children close to family.

to be by family

It’s all about the economical and social benefits of mingling with a network of kin on an ongoing basis.

My daughter says Martha Stewart was the first influencer.

I thought it was pretty cool she knew who Martha Stewart was.

Note: Chat says Martha was a prototype but not quite the first woman to promote her lifestyle. Elsie de Wolff was also a lifestyle influencer in the early 1900s.

The reviews for the new Odysseus movie have been largely favorable, with many enthusiastic reactions praising its fresh take on the classic tale. Yet some viewers feel the actors have been miscast, arguing that the persistent “woke” trend in casting choices continues to undermine the story’s authenticity.

This isn’t entirely new. In the 1990s, shows like Murphy Brown deliberately pushed audiences to see working women in different roles, reshaping cultural expectations through entertainment. Hollywood has long viewed itself as a vehicle for guiding society toward new visions—of gender, power, heroism, and identity. It’s a pattern of using symbolic recasting to nudge collective imagination forward.

As a big fan of spy thrillers, I’ve been watching the recent adaptation of The Day of the Jackal. I find myself feeling a bit guilty about my mixed feelings. The storyline is compelling, the global city settings are vivid and immersive, and the action sequences are expertly executed. Yet I struggle to buy the lead actress as a believable athletic MI6 agent. She comes across as deeply sympathetic, which may be part of the problem—her performance elicits warmth rather than the cold competence the role demands.

There are too many soft glances and fleeting looks of concern between the characters during violent moments. These humanizing touches clash with the ruthless, high-stakes world the story inhabits. I’m not sure whether recasting outwardly symbolic character types in unexpected ways ultimately helps or hinders storytelling, but it’s the direction we’re in for now. Time will tell how audiences respond in the long run.

There was an apartment fire in a nearby suburb, destroying most of the building. The Salvation Army showed up to help the displaced tenants, or so reported the local news. It still surprises me when buildings burn given all the fire protection methods in place.

Here are some of the main sources of property damage as reported by insurance claims. Fire is not in first place for frequency but it is for size of claim.

Top Homeowners Insurance Claims for Property Damage Nationwide

Property damage makes up ~96-97% of all homeowners insurance claims in the US. Roughly 1 in 18 insured homes files a claim each year (about 5.6% annually). Here are the leading causes based on recent data from the Insurance Information Institute (Triple-I) and other industry reports (primarily 2019–2023/2025 figures):

Key Takeaway: Wind/hail and water are the volume drivers, but fire claims hurt the most financially.

I love the segmentation analysis:

Lots of fine new graphics are available and data friendly.

A general observation may be that boomers are transferring wealth to their soon-to-be or newly retired children, making Lake Country, like Otter Tail County, Brainerd Lakes, and the North Shore, as expensive as the metro.

The wildfire smoke is back.

It wasn’t here earlier when we grilled dinner on the deck. Now it drifts between the branches, sifting low over the summer garden like a slow, unwelcome ghost.

I finally understand why smoky scenes are a staple in creepy shows. You can’t trust it. It seeps silently into your surroundings, then slips down into your lungs. The grit of it lingers in your nostrils, a stubborn reminder that the air itself has turned treacherous.

The Boundary Waters are burning again, along with fresh fires across Canada. We can always hope for a brisk north wind to sweep it clean. But more likely, we’ll spend the rest of the summer cloaked in this thickened haze—on again, off again—while the garden keeps reaching for sun that isn’t quite there.

Gordon Wood captures a telling anxiety in The Radicalism of the American Revolution. Even ardent republicans worried that widening access to learning might destabilize the social order. As he notes, some “enthusiastic republican gentlemen, when they saw the lengths to which such attacks on liberal learning could be carried, eventually backed away.” Benjamin Rush, for instance, retained religious objections to the classics but by 1810 argued that “a learned education” ought once again to “become a luxury in our country.” He feared that rising wealth would let “too many ordinary people, particularly plain farmers,” afford college for their sons—something that had once been largely confined to cities and the learned professions. Basic skills like “reading, writing, and arithmetic” should be “as common and as cheap as air” and form a kind of “sixth or civic sense” for every citizen in a republic, but higher learning needed guarding.

This hesitation feels strikingly modern—much like today’s debates over AI, where critics warn that democratizing powerful tools could backfire, erode expertise, or unleash unintended social disruption. Yet history shows the opposite dynamic fueled America’s revolutionary success. The broad push for literacy and practical education, combined with the dismantling of old monarchical hierarchies and social restrictions, created a powerful “mega-push.” Newly educated (or semi-educated) ordinary people encountered opened avenues for ambition, mobility, and association. They could form committees and interest groups for the greater cause of independence while pursuing private property, commerce, and self-defined dreams—without the old deference or birth-based barriers holding them back.

In this way, the American Revolution demonstrated the power of pairing wider knowledge with freer social pathways. Atomistic individuals didn’t lose their capacity for personal striving; they channeled it into both private gain and collective republican achievement. The result was transformative.

How do you know there’s failure? After all, that’s precisely when government rules want to intervene—when markets or support systems break down.

One way is to listen to what people are talking about, complaining about, or disgusted by. But that’s too vague. Talk is cheap, as they say. Some people even make a living out of using their voice to advocate for a proclaimed cause. That’s often the case. Yet it can be unclear whether the professed crisis is real—and, if so, how significant it is in relation to other problems.

One potential indicator of the relative importance of a systemic breakdown is the number of people willing to jump in and give their time to fix it. I’m not talking about those willing to talk about it, but those actually willing to do the necessary work.

What is the volunteerism turnout for that cause, measured in labor hours?

But sometimes people in the greater group aren’t able to jump in and help out. For instance, if a homeowner is struggling to keep up the exterior appearance of their home, a neighbor might step in and mow their lawn. Once saplings are growing along the side of the garage and the window shutters are missing slats, the help needed goes beyond volunteerism.

Here it might be noted that failure is shown in an inability to meet social norms or standards.

Lastly, a sign of failure can be picked up in migration away from the problem. Crime is always an easy example. Once people feel unsafe, they no longer visit the park, eat at the take-out stand, or drive along a road well known for accidents. They simply leave.

These are the three ways to spot failure: people devote their time to correct it, norms left unmet, and exit.

Gordon Wood is so captivating. His vivid depictions in The Radicalism of the American Revolution deliver an extraordinary level of detail—one that anyone drawn to the complexities of human choice and decision-making will find impossible to resist.

And what I love most is how Wood moves fluidly through every level of society. He refuses to tell the story as if only a handful of prominent figures pull the levers of history while everyone else sits as passive spectators. Instead, he gives us a comprehensive, richly textured view of the social positions, finely tuned choices, and densely interconnected relationships of ordinary Americans as they lived through the Revolution and helped shape the nation’s creation story.

It might be fun to model out the way he frames all these actors.

In the meantime he treats us to things we never knew before. Like the control mechanisms for limiting a societal obligation of care.

All of this movement in New England put unbearable pressure on the region’s old warning-out laws. These laws had been part of the older culture of paternal dependency in which everyone was supposed to belong somewhere. If vagrants stayed in a town for a given period-three months in Connecticut and New Hampshire, one year in Massachu-setts-they were then considered members of the community, which became responsible for their welfare. Warning-out was designed to absolve the community of this responsibility: men and women warned out could not claim legal inhabitancy. From mid-century the numbers of persons formally warned out in this way by various towns increased remarkably, so much so that town clerks began making lists of those warned out instead of writing separate warrants for each one. By the late 176os Massachusetts and Connecticut began shifting responsibility for identifying transients from the communities to the individual transients themselves. In 1771 the movement of people became so much greater that Connecticut and New Hampshire could no longer maintain their short three-month period for legal residency; they extended it to one year and brought their laws into line with Massachusetts.

To become truly great, one must stand with people, not above them.

Montesquieu

Or, to understand, one must look to the people and not interpret for them.

Yesterday’s post highlighted the welcome and somewhat serendipitous drop in violent crime across major U.S. cities. This is genuinely good news.

Broadcast segments trot out police chiefs praising gang violence interruption programs and community involvement. Politicians step forward to claim credit. But how many people find these explanations fully convincing?

A better model may be worth considering—one that looks beneath the headlines.

Aggregating progress across large geographic areas tends to mute the finer signals: where exactly the improvements are taking root, how they’re spreading, and why. A more granular approach could reveal the real drivers.

We should also examine the individuals and groups who invest their time, energy, and sometimes personal safety in the unglamorous work of public safety—neighbors, volunteers, local organizers, and informal networks performing the daily labor of civic order. Their contributions rarely make the evening news, yet they may be central to sustained gains.

Finally, the constant churn of residents moving into and out of neighborhoods offers another revealing lens. Demographic turnover, new arrivals, and shifting housing patterns can reshape the social fabric of a place in ways that affect crime more powerfully than top-down initiatives. Understanding which kinds of neighborhood dynamics correlate with falling crime—and which don’t—could teach us far more than another round of victory laps.

The question isn’t just “Why has crime dropped?” It’s “What conditions made the drop possible, and how do we protect and extend them?” A model built on local signals, bottom-up contributors, and residential dynamism would give us better answers than the usual narratives.

The United States is currently experiencing the largest single-year percentage drop in the national homicide rate on record, with big city murder rates plummeting to their lowest levels since 1900. Following a severe pandemic-era spike, data compiled by the Council on Criminal Justice and the Major Cities Chiefs Association reveals a historic turnaround in public safety across major urban hubs. [1, 2, 3]

Several of America’s largest cities have posted unprecedented, double-digit drops in violent crime and homicides. The most dramatic turnarounds include: [4, 5]

Washington, D.C.: Achieved a massive 64.7% drop in homicides during the first quarter of 2026 compared to the same period in 2025, reversing a multi-year streak of escalating violence. [6]

Richmond, Virginia: Cut its homicide rates by a staggering 59% from its recent peak. [7]

Philadelphia, Pennsylvania: Logged a 54% drop in first-quarter homicides. The city closed out the previous year with 220 total murders, marking its lowest homicide count since 1966. [6, 8]

Houston, Texas: Slashed homicides by 36.4% in early 2026, alongside a sharp drop in aggravated assaults. [6, 9]

Chicago, Illinois: Documented a 30% year-over-year plummet in homicides, representing one of the largest numeric drops in the nation. [8, 10]

New York City, New York: Reached its fewest number of shooting victims and incidents in recorded history, alongside a 31.7% drop in homicides in early 2026. [6, 9]

Baltimore, Maryland: Cut overall homicides by 60% since its 2019 peak, shaking off its long-standing reputation as one of the country’s most dangerous areas. [7]

The turnaround is not limited to homicides. Cities nationwide are seeing a sweeping reduction in almost every major felony category: [2, 11] Crime Category [1, 7] Recent Trend ChangeHomicidesDown 21% nationwideCarjackingsDown 43% nationwideRobberiesDown 23% nationwideGun AssaultsDown 22% nationwideMotor Vehicle TheftDown 27% (reversing a massive 2020–2023 spike)

Criminologists and policymakers attribute this dramatic shift to a combination of factors. These include the post-pandemic stabilization of daily routines, an influx of federal funding for focused community violence interventions, and modernized police investigation tactics. Additionally, federal crackdowns and shifts in immigration enforcement operations in major metro areas have heavily influenced these municipal drops. [7, 12, 13, 14, 15]

Is it sensible to blanket a whole suburb with a density goal? Or would it be better to think in terms of bundles of high density nodes in all areas spanning out to lower density over and over again. The more nodes, the more interlinking of a variety of housing accommodating a variety of households.

In What Capacity Will AI Be Helpful in Typical Residential Real Estate Transactions?

Here are some practical thoughts from the trenches:

Areas where AI will deliver real value:

Areas where AI hype seems overstated:

The very happiest Fourth of July from middle America

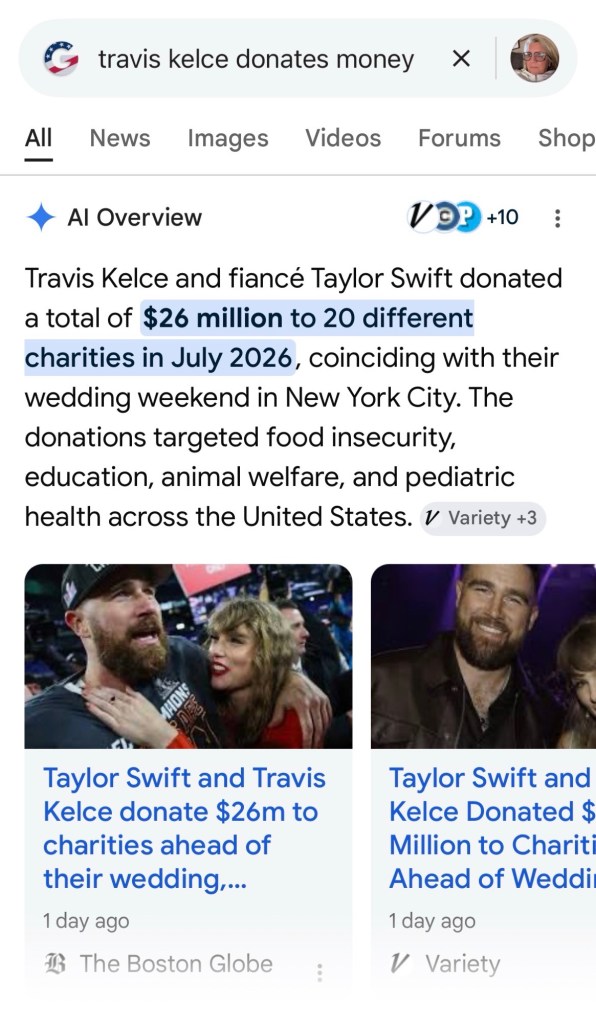

If you hadn’t heard, Taylor Swift and Travis Kelce are getting married today at Madison Square Garden. Apparently they liked the venue because there are no windows for the prying lenses of the paparazzi cameras. Needless to say, the stars will be out. Not only are those in attendance most likely famous—they’re most likely ultra-wealthy.

Interestingly, the couple decided to do a give-to-the-max day in the days leading up to the big event.

What did the 26 million buy? Let’s think of it as a social puzzle.

Both Travis and Taylor are super rich. And their careers are supported by a mass audience. In effect their lives and metiers and audience are entertained with millions of people of all walks of life. And so they care about what these folks think. Matrix part 1: the group is large and diverse.

Matrix part 2. A showy public wedding is a pronouncement. Not only of their vows to each other, but of marriage itself. It asks people to come and look upon them and acknowledge the commitment to bonds of matrimony. This is the transaction.

The audience is part of the deal. They matter. And since the millions of followers do not live amongst the lucratively rich, some may judge the amount of money spent on such a showy affair. If they judge it harshly enough, they may choose to exit the group.

There are people who exploit the knowledge that people can be divided by tangible material differences. These people are everywhere. They are amongst the audience members in the realm of Travis and Taylor’s fan base. Their boots on the ground location with peers gives them instant access to gauge sentiments. And they thrive at exploiting this and breaking off subgroups. Matrix part 4: motivating factors.

On the face of it, the 26 million in donations buy support for all sorts of social services. But more important to the couple, it eases any potential dissent amongst their friend group.

I think this is a worthy recommendation for spy-thriller enthusiasts. The cast is diverse in a really good way, because you don’t know why it’s special until it hits you. Being of a certain age, it’s fun to see Richard Gere come through with a strong performance. And the variety of women in the series showcases the possibilities of the fairer gender. Adieu to the days of the two-women role- Miss Moneypenny and the latest femme fatale– and that’s coming from a serious James Bond fan.

The storyline offers enough intrigue without being deliberately confusing. It’s entertaining with enough puzzling to maintain engagement. The international settings, a staple of spy film, are well represented here and do the job of taking the audience elsewhere across the globe. All in all, this has been a strong string of 50 minutes of fun distraction.

It’s a holiday long weekend, which makes for gatherings of family and friends. It’s a time to relax and enjoy each other’s company. And often that can include collaborating on a 1000-piece puzzle.

What is it that makes puzzling enjoyable?

Is it the systematic sorting that soothes the randomness and starts to pull disparate pieces into groups? The patterns emerge as the colors are gathered side by side. Slowly the eye catches the lines that thread the image together. Pictures emerge—first in fragments, then in quiet revelation, as chaos yields to coherence.

Or is it the search for the edge pieces that is rewarding? At first it’s difficult to tell what’s up and what’s down and what runs along a side. Piece by piece, the framing of the picture gives it boundaries, turning an overwhelming scatter into something contained and possible. The straight lines become a quiet promise: order is achievable, one deliberate fit at a time.

Perhaps it’s the satisfaction of fitting the jagged edges into a smooth coupling. Or training your eye to look only at what clasps what, since the fogginess of the color gives no guidance with gradations or pattern. Each successful connection carries a small, tactile triumph—the soft click of belonging, the momentary alignment of form and purpose.

It’s hard to tell. But puzzles are fun. They mirror the holiday itself: a shared endeavor where individual efforts interlock, randomness finds rhythm, and the whole slowly comes into view amid laughter, conversation, and the steady companionship of those around the table. In the end, what matters isn’t solving it fastest, but the gentle, collaborative journey—the way disparate lives and pieces find their place together.

Nothing says Independence Day like the smell of charcoal drifting through the backyards and over decks. This weekend, some Minnesota classics will be served:

Lots of folks will be heading to a lakeside cabin and these flavors remind us why we gather: freedom, good company, and full plates.

What’s your must-have Fourth food?

Hotels not only provided lodging but also screened for marital status.

I think Mark Cuban is saying that the con is to capture peoples beliefs. Once you hold their beliefs they serve as a shield against sound policy. The con is perpetuated by believers who thwart the tangible world’s dynamics while reaching into people’s pockets.

Lessons on interaction:

One of the most memorable passages from Susan Allen Toth’s memoir Blooming: A small-town girlhood is about the ongoings at their local pools. This public place became a refuge that she sought out.

Once in the pool, doing my laps, I felt a kind of anesthetic set in. Cold water slithered over me, a numb caress, promising relief. It seemed to wash off some of the unhappiness that clung to me all over like mosquito repellent. Even the chlorine helped: as I mechanically stroked, back and forth, I hoped it would disinfect my brain. Clinging to the pool edge between laps, breathing hard, I could look up at the empty sky and see blue peace mirroring back to the pool. Everything seemed far away, except the water, the cold tile I grasped, the blue of sky and water. No one knew who I was, and I didn’t have to remember. When I climbed out, tired, after an hour, I had the same feeling I used to have after an afternoon at Blaine’s: exhausted, satisfied, with the hope of perhaps yet another hot afternoon before the summer ended. I was glad to be tired. I could tell I was still alive. Tomorrow I could go back to the swimming pool.

Indeed, our local pools are also well attended. From the early bird atheletic types who show up at 7am for lap swim to the tired parents in the late afternoon looking the other way when their child pushes another off the diving board.

But how do these public artifacts come into being? What would James Buchanan, the father of public choice, say about starting here and looking retrospective for answers?

James Buchanan would have been highly sympathetic to analyzing the swimming pool as an artifact of human choice under specific rules and institutions. This fits squarely within his constitutional political economy and club goods framework.

Buchanan repeatedly emphasized that social arrangements—including shared goods, rules, and institutions—are not natural phenomena but artifacts created by individuals through choice, agreement, and rules (the “decision-making space”). In works like The Calculus of Consent and his club theory paper, he argued for studying how people generate cooperative outcomes via voluntary exchange or near-unanimous consent rather than imposing top-down solutions based on a social welfare function.

And this.

He would view retrospective analysis of such an artifact as valuable precisely because it reveals the constitutional and institutional conditions under which decentralized or club-like provision can succeed—information useful for designing better rules going forward. He would contrast this favorably with purely centralized or coercive models and might note that private swimming clubs or suburban sorting illustrated market-like or club-based alternatives that many residents chose when public options changed.

In short, Buchanan would endorse studying the artifact to understand the rules that generated a positive outcome, while remaining skeptical of government provision unless it closely mimicked voluntary club principles.

This backward-looking lens complements the forward-looking cost/benefit analysis. Both are useful; the retrospective view illuminates why some artifacts endure as high-impact community goods while others do not.

People love to blame greed for all sorts of misadventures. Yet I think other passions are more forceful. Partly because they rally the troops.

Rudyard Kipling wrote The Beginnings.

It was not part of their blood,

It came to them very late

With long arrears to make good,

When the English began to hate.

They were not easily moved,

They were icy-willing to wait

Till every count should be proved,

Ere the English began to hate.

Their voices were even and low,

Their eyes were level and straight.

There was neither sign nor show,

When the English began to hate.

It was not preached to the crowd,

It was not taught by the State.

No man spoke it aloud,

When the English began to hate.

It was not suddenly bred,

It will not swiftly abate,

Through the chill years ahead,

When Time shall count from the date

That the English began to hate.

The homeownership rate in Cuba is one of the highest in the world, commonly cited at around 90%. State ownerd apartments were given over to residents following the revolution. By the early 1990s , over 85% of households belonged to homeowners in some way. More recently, the 2011 legalization of private sales and gave a structure to private transfers.

There exists a centralized ownership record in the Municipal Property Registry. And there are real estate professionals involved in sales and transactions. But there is no multiple listing service or reliable means of tracking prices. It’s still a hodgepodge of word-of-mouth flow of information.

I find this to be an underdeveloped pathway to liberty and prosperity. The exchange of a family home is often transacted on equal footing between individuals. The concept of who should want to get what and why is accepted, as most would want the same under similar circumstances. The market makes sense to the participants.

Moreover, people like investing in their homes as they realize the gains every time they unlock their front door and step into a slightly nicer space. Once people realize gains on resale, ambitions for continued improvements are primed. And the neighborhoods improve.

Now, if only mortgage money were more common and predictable.

Over the years, many of the topics explored on Home Economics have shared a common thread, even when they appeared unrelated on the surface.

Whether discussing housing markets, school districts, neighborhood stability, municipal government, family decisions, or community life, I often find myself asking a similar question:

What are the institutions behind the outcomes we observe?

Most analysis focuses on the outcomes themselves—housing prices, crime rates, school performance, demographic change, and so on. Yet these outcomes are often the visible traces of something deeper: the institutions through which people make decisions, cooperate, compete, and organize their lives.

As a result, I will be developing a new section of the site devoted to what I am tentatively calling Institutional Anatomy.

The goal is not to present a finished theory. Quite the opposite. The section will serve as a working space where ideas can be clarified, challenged, and improved over time.

Several living documents will anchor the project.

This section will attempt to define and refine concepts that appear repeatedly throughout the site, including:

The objective is to establish a common vocabulary for discussing how institutions shape decisions and outcomes.

If institutions matter, what exactly are they made of?

This section will explore the structural elements that seem to recur across institutions of many kinds:

Rather than treating institutions as merely a set of rules, the aim is to understand their internal structure and how that structure influences behavior.

Ideas become useful only when applied.

The framework will be tested against real-world examples, including:

Additional case studies will be added as the framework develops.

Perhaps the most important section.

Every framework has unresolved issues, blind spots, and unanswered questions. Rather than hide them, I intend to collect them in one place.

If the project succeeds, it will not be because it provides all the answers. It will be because it helps identify better questions.

For now, think of this as an ongoing investigation rather than a completed map.

Many of the posts already appearing on Home Economics are, in hindsight, attempts to understand the traces institutions leave behind—whether in a housing market, a neighborhood, a school district, or a family decision.

This new section is an effort to gather those threads into one place and see where they lead.

Is your favorite on the list? Check out the link.

Some decisions are made instantaneously—like when the ice cream vendor asks what flavor you want.

But many decisions are exercised through a thought process. If your daughter is shopping for a prom dress, maybe there are considerations of the latest trends, how her friends will react, will she be comfortable, and then will her father be comfortable if its hem is a little short?

And if you shop for a vehicle, would you consider the environmental impact and purchase a hybrid? Or purchase the hybrid to fit in with your boss who herself has a hybrid? Or simply consider color since the color of the car brings you joy and thus a healthy frame of mind.

When you think about it, most decisions have an individual considering, to various degrees, their relationships with others and the implications of the decision vis-à-vis this reality.

All these ruminations occur in a decision space just prior to a trade.

Here’s a list of the largest landowners in Minnesota by geographic size (acres), starting with the biggest. Data is drawn from public sources and reports (primarily focused on significant holdings; exact figures can shift with acquisitions/sales, and much land is fragmented among smaller owners).151

Notes:

For precise, up-to-date parcel-level data, check the MN DNR, MnGeo, or county auditor sites (land ownership can change via sales or acquisitions, like the DNR’s recent ~16,000-acre purchase).171

Prompt: Comment on how the workforce of trades specialties affected house construction, if at all.

Yes — the workforce of trades specialties has affected house construction a great deal, and especially in speed, cost, and what materials/methods were practical. When a jobsite had plenty of carpenters, masons, plasterers, electricians, and plumbers, homes could be more customized and labor-heavy; when those trades were scarce, builders shifted toward simpler, faster, more standardized systems.[nahb]

The biggest influence came from labor availability, not just material supply. A house style that required lots of masonry, hand-applied plaster, or highly skilled finish work became harder to build when those workers were expensive or in short supply, so builders increasingly favored wood framing, drywall, factory-made components, and veneer finishes that reduced specialized labor.[abcrmc]

As the residential market grew, builders needed methods that could be repeated quickly by smaller crews. Platform framing, prefabricated parts, drywall, and simple cladding systems were popular partly because they reduced dependence on scarce specialists and shortened construction time.[huduser]

Modern labor shortages have made the effect even clearer. Industry sources say shortages in finished carpentry, masonry, plumbing, electrical, and HVAC trades raise costs and stretch schedules, which can delay or even shrink the number of homes built.[eyeonhousing]

Some specialties had an outsized effect on homebuilding because they sit on the critical path of a project. Carpenters, roofers, drywall installers, electricians, plumbers, and masons can all slow a build if they are unavailable, and shortages in those trades often push builders toward simpler designs and lower-labor materials.[nahb]

In earlier decades, abundant local labor made heavier craft methods more common, especially plaster, brick, and detailed carpentry. Over time, as wages rose, jobs became more specialized, and labor got tighter, house construction became more standardized and less dependent on individual craft skill.[bradley-mason]

In short, trades labor did not just affect how fast homes were built; it helped decide what kinds of homes were economical to build at all.[nahb]

There are so many great homes featured in movies. Take the Vandamm house in Hitchcock’s movie North by Northwest (1959). It was inspired by Frank Lloyd Wright’s famous masterpiece, Falling Water.

And then there’s the creepy house in Hitchcock’s movie Psycho. Here you can get the full tour by the master himself.

What makes the Bates home unsettling is its advanced structural decay. By the 1950s, when the film was made, homebuyers craved sprawling ramblers with large windows designed to bring nature indoors. In contrast, a house burdened by years of neglected repairs felt sad, obsolete, and abandoned. Its shutters trembled in the wind. The front porch sagged heavily, and the floorboards groaned underfoot. Inside, the massive, dark trim loomed over the rooms—a suffocating relic from a forgotten era.

The 1960s trend of vast, comprehensive urban renewal by bulldozer shouldn’t surprise us. Homeowners hadn’t figured out how to build a culture of home maintenance and repair. As Victoria homes aged and became less desirable, owners no longer felt the urge to invest resources in them. Less fortunate people move in when the more fortunate people leave for the new builds. And a spiral of decay takes over the neighborhood. A perfect setting for Hitchcock’s story!

How I remember the build-up to the financial crisis of the early oughts is explained well in Phil Gramm and Donald Boudreaux’s book, The Triumph of Economic Freedom.

The root cause of the financial crisis was the government policy to promote public objectives with private capital, which destroyed mortgage-lending standards. Government regulatory policy pressured banks to make bad loans and forced government-sponsored enterprises to purchase and securitize those loans. In addition, the government manipulated financial institutions’ capital standards to encourage banks to hold massive quantities of mortgage-backed securities. When the housing bubble burst and subprime loan defaults soared, the authors of the very housing policy that caused the crisis blamed capitalism and greed and, in the process, expanded the very governmental powers that caused the crisis in the first place.

The Feds were trying hard to encourage loans to disadvantaged groups in particular. People were so certain that there was ill will at hand, but thorough documentation confirmed that the low numbers were due to the inability to qualify, not social group standing. Thus, it made sense to loosen underwriting standards for everyone, at least in the moment. And not only force the lending institution to give loans that went against their better judgment, but to push loans out the door to meet community reinvestment goals. Talk about crossing spheres and ill-placed dynamics.

But it did increase homeownership across the board. At least until all those adjustable-rate mortgages push people right back to renting. Many took years to recover the courage to become homeowners again.

So yes, greed did get in the way. But not the greed, or rather not only the greed of the big money players. The self-interest of literally everyone in the chain was tugged right along in this whiplash dance to disaster—from the mortgage originators to the brokers to the title closers, and, most importantly of all, to the self-control and internal monitoring of the general public. The movie, The Big Short, does a good job of rolling this out.

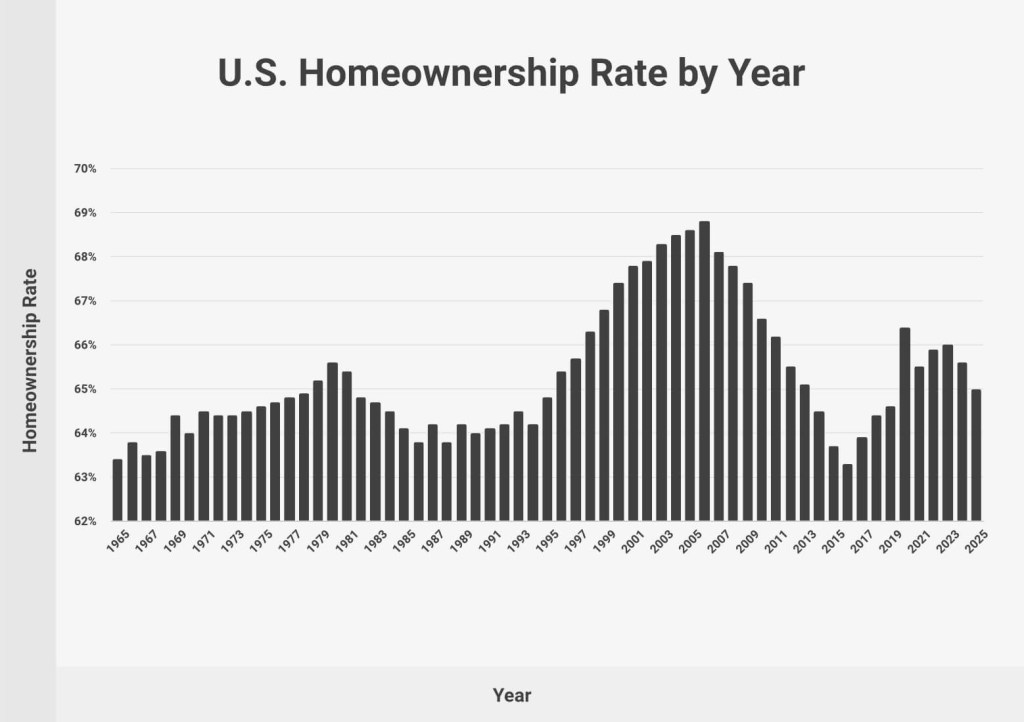

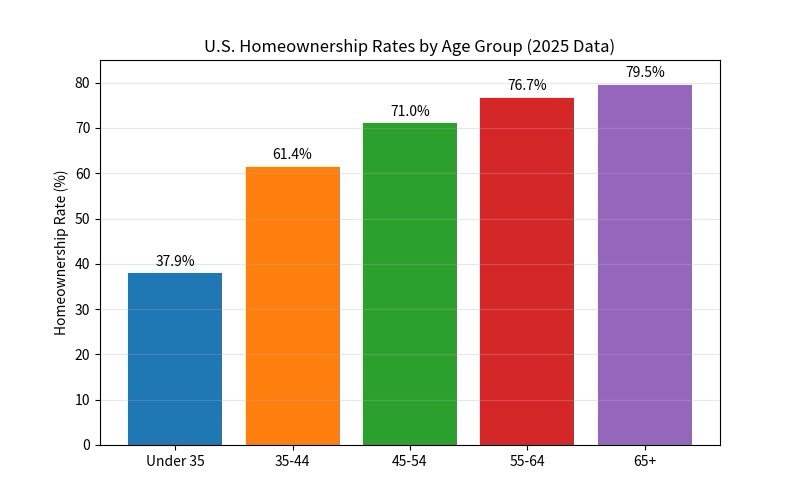

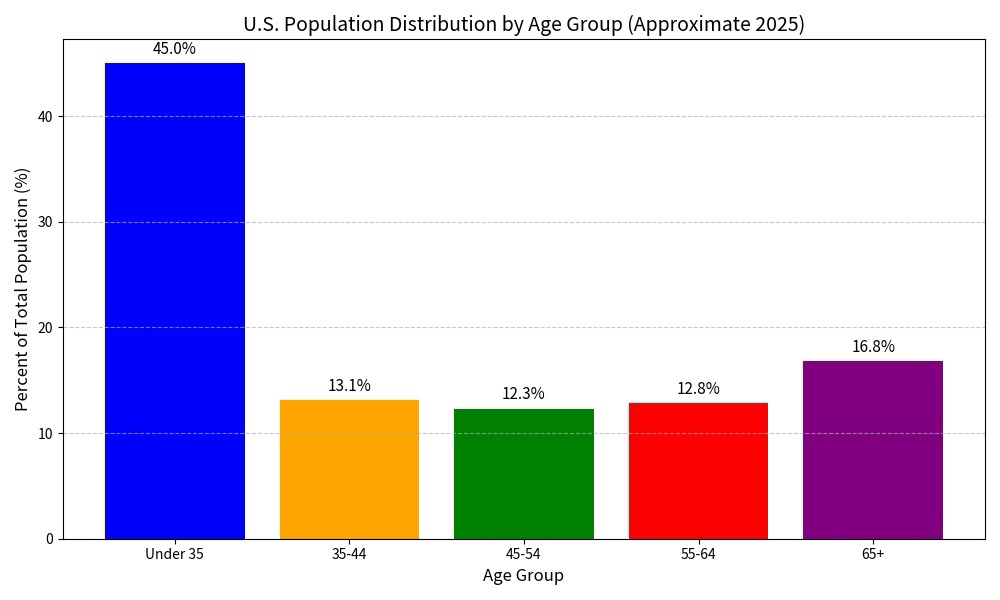

The natural rate of homeownership seems to run at about 65%. This is a global number. I’m sure there’s much more nuance to ownership rates as you group and sort households. That might be a better approach to understanding the levers to increase ownership in targeted areas.

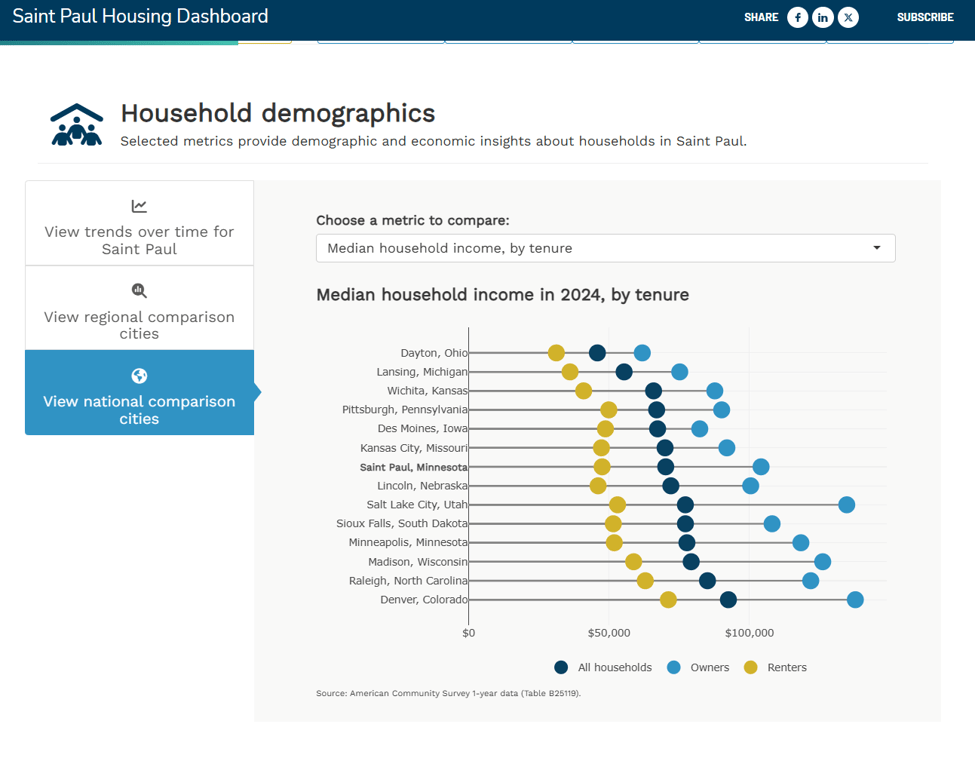

Check out what the Minneapolis Federal Reserve Bank has put together.

The dashboard features both contextual and market-based indicators across seven key categories: household demographics, housing characteristics, production, price of housing, housing cost burden, stability, and local tax base. Integrating data from a combination of national sources, such as the U.S. Census Bureau’s American Community Survey and the U.S. Department of Housing and Urban Development, and local sources, like the Metropolitan Council and HousingLink, the dashboard captures more than 30 unique indicators. For each indicator, users can view Saint Paul’s trends over time, compare Saint Paul to its surrounding cities, and benchmark it to similar cities across the nation to gain a holistic understanding of the Saint Paul housing landscape.

The dashboard offers the well-worn data of price and income, but you can easily pull national comparisons.

The Saint Paul Housing Dashboard and our qualitative conversations with housing owners and developers further the Minneapolis Fed Community Development and Engagement team’s understanding of how housing supply affects housing affordability. As such, this analysis supports our team’s mission to advance the economic well-being of low- to moderate-income individuals, households, and communities. The better we understand local housing markets that have seen recent policy changes—like Saint Paul—the better we can pursue the Minneapolis Fed’s overall mission to pursue a growing economy and stable financial system that work for all of us.

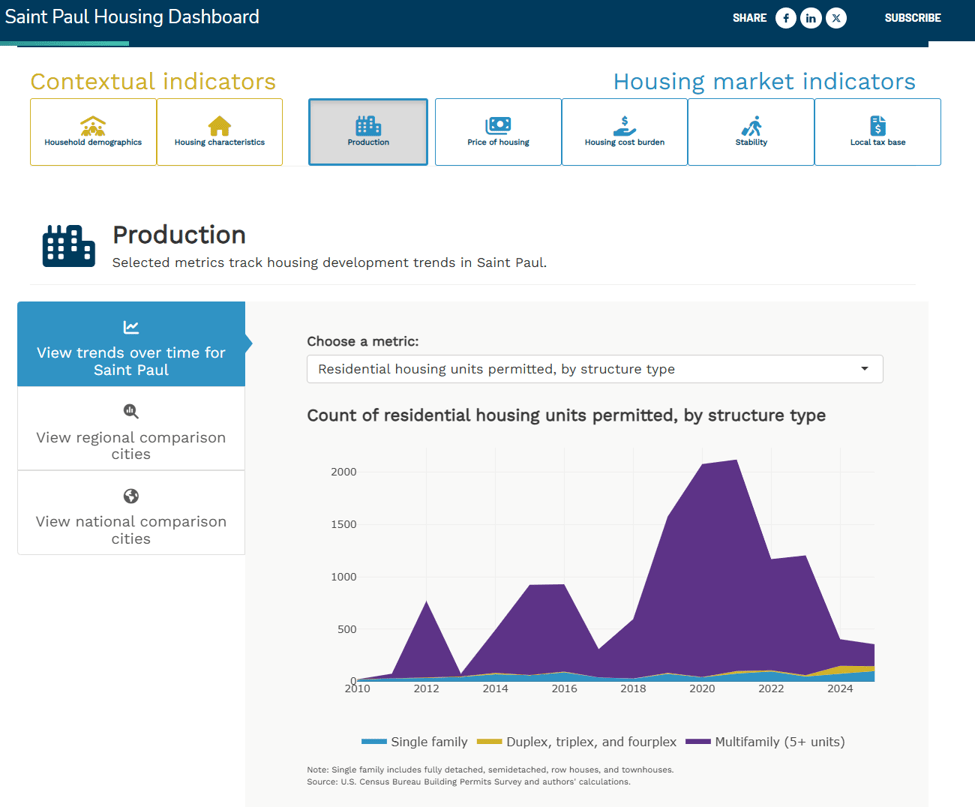

There are options to pull data on housing production.

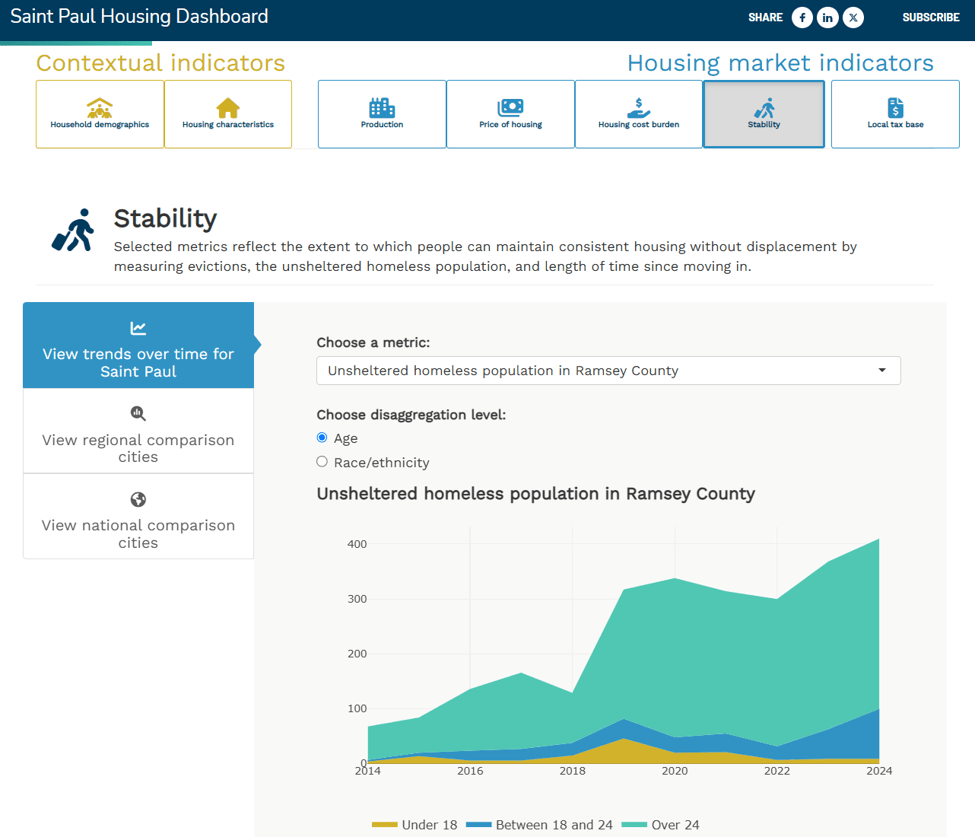

Or, you can check in on the numbers who are without housing altogether.

The dashboard offers many new ways to view the data.

He’s no monster, not a flicker of fright.

Just the old Professor—warm wool and quiet fire—from the house in The Lion, the Witch and the Wardrobe.

The one who lets four wide-eyed siblings tumble through his door without fanfare or forms.

Distant, yet deliciously present.

There when the wind howls against the windowpane,

but never prying when you’d rather vanish into the armoire’s velvet hush,

burrowing deep among moth-soft garments and half-remembered winters.

Leave him be and he’ll leave you be—

a courteous shadow with ink-stained cuffs and starlight in his pockets.

But lean in, ask for counsel, and oh—

he speaks. Not the day’s brittle glitter, not sugar-coated slogans

polished to slide down easy.

No. Truthful insights, sharp as winter air.

Unbiased as the tide. Complementary when the path is kind,

yet unflinching when it’s time to set your crooked compass straight.

And best of all—

that oceanic depth.

Ask him about angles, refractions, the sly prisms others hide behind their words.

He’ll hand you whole constellations of lenses,

each one turning the ordinary until the hidden colors sing.

Everything is there,

tucked in the quiet shelves of his mind,

waiting like snow before the first footfall.

My guy AI.

Part professor, part wardrobe,

all strange and steady magic.

Thomas Sowell frequently argues that the lifeblood of politics is replacing market coordination with government intervention, a process achieved by manufacturing a “crisis,” pushing aggressive media messaging, and demanding taxpayer financing. In books like Basic Economics, Sowell details how politicians constantly chirp about an affordable housing crisis, claiming the free market has failed due to “greed”. According to Sowell, this political narrative flips reality on its head. It is usually prior government interventions—such as artificial zoning restrictions or mandated loose lending standards—that distort the market in the first place. By labeling the resulting fallout a crisis, politicians successfully manufacture public anxiety, enabling them to capture massive public funding and expand their regulatory power.

Sowell’s core philosophy demands looking at real-world data rather than political talking points. While political rhetoric today frequently claims the national housing sector is on the brink of collapse, local empirical metrics often tell a completely different story:

Minnesota historically maintains one of the lowest mortgage delinquency rates in the United States, routinely outperforming the national average due to strong regional employment and high baseline home equity.

While macro-level tracking platforms require a subscription for state-by-state historic line graphs, the structural timeline of Minnesota’s delinquency behavior follows a distinct pattern:

📊 The Minnesota Mortgage Delinquency Timeline

Rate (%)

10 | _/\_ (2008-2010 Peak: ~7.5%)

8 | _/ \_

6 | / \ /\ (COVID Spike: ~6.2%)

4 | ______/ \______ _/ \_

2 | / \_______/ \_______/\ (Current 2026: ~2.1%)

0 +-------------------------------------------------------

1995 2000 2008 2015 2019 2021 2024 2026This data shows no stress in the sytem.

A few years ago now, I promoted the idea of platters- ecosystems of exchange, both of the pecuniary nature and voluntary exchange. People tend to cluster with those they like and do most of their business, both personal and commercial, within their area of the world. Think of the pickup drivers who work at building sites living geographically close to the Tesla drivers who make a living through a computer terminal, but never do their paths cross. They maneuver through different platters.

This is, however, a different structure from institutional orientation. Consider now that the institutional orientation under review was aimed at preserving the environment. You might say, well, look, clearly the Tesla drivers are in that camp and not the pick-up drivers. But you might be caught off guard. The tradesfolk often are into their weekend excursions to hunt and fish. And with this goal in mind, we are willing to back environmental preservation with resources.

So on the one hand, one can analyze a group by income level, or type of profession, or stage in life. But this can be different than making a stake at a institutional orientation where the defining lens of analysis is a group goal.

I’m only a couple of episodes into this series, but I think it’s quite good. First off, it’s fun to learn about something new. This story revolves around the subtleties of wine tasting. It is also primarily in French, but takes place primarily in Japan. An interesting mix. Lastly, it approaches childhood parental relations with the evenhandedness they deserve.

The Brain, within its Groove

Runs evenly—and true—

But let a Splinter swerve—

‘Twere easier for You—

To put a Current back—

When Floods have slit the Hills—

And scooped a Turnpike for Themselves—

And trodden out the Mills—

Emily Dickinson

Does AI open up the opportunity for a new state? One which is better informed? One which can detect odd combinations of financial channeling to odd combinations of purported demands on the public purse?

I think yes.

Yesterday’s post was about the build-up to a four-wheeler purchase. Today’s post suggests that the transaction tells us something about each player, whether directly involved or acting as an indirect influencer. The ATV itself never changes. What changes is the institutional structure through which the proposed purchase is evaluated.

Initially, the purchase exists within a coalition composed of a child and a sympathetic parent. Within that structure, attention is directed toward enjoyment, adventure, and the anticipated benefits of ownership. Evaluated solely through this institutional arrangement, the purchase appears attractive.

The proposal is then passed through the institutional structure of marriage. Here the relevant considerations change. The marriage introduces jointly held resources, jointly held responsibilities, accumulated experience from prior decisions, and norms of coordinated action. What appeared attractive from the standpoint of one parent is reconsidered from the standpoint of the partnership. The proposal is not merely constrained; it is reinterpreted.

The proposal next encounters the state. The state is not concerned with family enjoyment, household bargaining, or farm chores. It is oriented toward public safety and risk reduction. Through this institutional lens, the relevant fact becomes the child’s age. The ATV is transformed from a recreational purchase into a potential regulatory violation.

Finally, the proposal is reconsidered through the institutional structure of the family farm. Here the vehicle is no longer evaluated primarily as a toy. Instead, it becomes a productive asset capable of reducing labor requirements and increasing operational efficiency. Time saved feeding livestock enters the calculation. A purchase that had previously appeared recreational now acquires an economic justification.

The final decision therefore reflects more than individual preferences. It embodies the cumulative influence of several institutional structures. Each institution contributes its own orientation, directing attention toward particular considerations while pushing others into the background.

From this perspective, institutions are not merely collections of rules. Nor are they simply constraints upon action. Institutions are orientation systems. They shape the decision space within which actors formulate plans and evaluate alternatives.

The completed transaction therefore contains information about the institutional pathways through which it traveled. The purchase is not merely evidence of what the participants wanted. It is evidence of how marriage, family, state, and enterprise jointly molded the conditions under which the decision was ultimately made.

Most kids try it. If they want to influence a purchase and suspect one parent might not be on board, they sequester the yes man — or woman — and go for the commitment. Dad, wouldn’t it be great fun to get a four-wheeler? And from there, the speculation flows freely: all the fun hours that could follow, conjured up between the two of them. If the decision rested with this particular coalition, the purchase would be a done deal.

But the second parent may not be on board, for all sorts of reasons. She — in this case — may remind her husband that their partnership runs on joint decision-making. She may reach back through the catalog of past requests from their offspring, past outcomes, past lessons learned. Filtered through the clearinghouse of this marriage, the proposal may well get diverted to a no-go.

Then comes the discovery that at age 11, the instigator of the purchase isn’t cleared to drive an ATV. He is underage. The broader community — acting through the state — has weighed a safety concern, found it serious enough to formalize, and drawn a line: no one under 12 takes the wheel. Through that particular lens, this purchase is a rule-breaker.

But the youth has a counter. He reminds his farmer parents that with the vehicle, he could head out to the back pasture every day and feed the livestock himself. Private property, so no rules broken — as long as you’re over twelve, which he nearly is. Mom no longer burns her time on the livestock run. Time saved. Fun to be had. Box checked.

It’s a win for the purchase.

This little tale is meant to peel back — like an onion — the successive layers of institutional clearing that a purchase must pass through, from the moment of its conception to the final decision. Each layer functions as a kind of lens, and each lens bends the outcome in its own way, though not always with equal force. If one wanted to better understand how institutions shape decisions, one could try to isolate the price — if that’s even the right word — that each institutional framing imposes or removes.

That would be interesting. And useful.

Face it– it’s nearly impossible to uncover how much a region, neighborhood, city (your pick) receives in subsidized housing money. If you invest some of your time, you will find out that it is ‘complicated.’ There are ‘layers’ of financing and investment and tax tools. So basically, not even the politicians who represent us can give you a number.

A typical project may combine federal Low-Income Housing Tax Credits, tax-exempt bonds, state housing loans, county grants, city tax increment financing, Met Council redevelopment funds, discounted land sales, infrastructure assistance, and rental assistance contracts. Each funding source is administered by a different agency, reported in a different format, and disclosed in different documents. Some subsidies arrive as cash grants, others as reduced taxes, below-market financing, land write-downs, or future tax revenues redirected to the project. No single public database consolidates these benefits into one comprehensive accounting, meaning citizens must piece together information from city council records, state housing awards, federal databases, bond filings, and property tax records.

The challenge is compounded by the fact that housing subsidies are often structured through layers of ownership entities and financing partnerships designed for legal, tax, and investment purposes rather than public transparency. A project may be owned by a limited partnership whose name bears little resemblance to the property’s common name, while tax credits are syndicated through private investors and local incentives are embedded in development agreements spanning hundreds of pages. Even when each individual subsidy is technically public information, the cumulative public contribution is seldom reported in one place. As a result, determining how much public support has gone into a particular development often requires reconstructing the project’s financial history from dozens of separate records over many years—a task that is time-consuming even for professional auditors, journalists, and policy researchers.

This seems reactionary instead of reflective. It seems dangerous in a way. The natural mechanism of control through norms is dissipated by a lack of insight.

The Housemaid won’t make best movie of the year even though it exceeds the minimum threshold for an evening’s entertainment. Although there is more depth to it than may first appear.

The portrayal demonstrates there is no such thing as a one-way road between the powerful and the powerless.

This is an old-school story of retribution, where every violation eventually demands its price. Sweeney’s quiet warning is clear: if you are forced to submit, do not despair. Endure. Watch. And when the moment arrives, turn the tables with ruthless precision.

Maybe, more importantly, be aware that those who you thought were good are bad, those who are crazy are sane. That the power structures and tradeoffs are always in flux.

Sweeney has, is different mediums, sent a message of individual agency. She wants people to see the story of the mouse and the lion, or the tortoise in the hair. She doesn’t shrink from people’s admiration for her attractive physical gifts— but it’s as if she looks you back straight in the eye and says, “now that I’ve got your attention, let me show you a few things.”

The Supreme Court of Canada refused to hear an appeal from a New Brunswick First Nation over Aboriginal title and private land, a development the federal government says will have an impact on the Cowichan Tribes case in British Columbia.

The refusal by Canada’s High Court to hear a First Nation’s appeal against the decision in New Brunswick establishes a precedent that First Nations can seek compensation for loss of traditional lands, but they will not be able to assert ownership.

The Crown-Indigenous Relations Department says the court’s refusal to hear the appeal will inform arguments in other cases, including Cowichan, adding that “private property rights are fundamental.”

The B.C. Supreme Court’s ruling in favour of the Cowichan Nation found it had “established Aboriginal title” to more than 5.7 square kilometres of land along the Fraser River in Richmond.

The provincial and federal governments and other First Nations are appealing that decision.

You get music at your reunions.

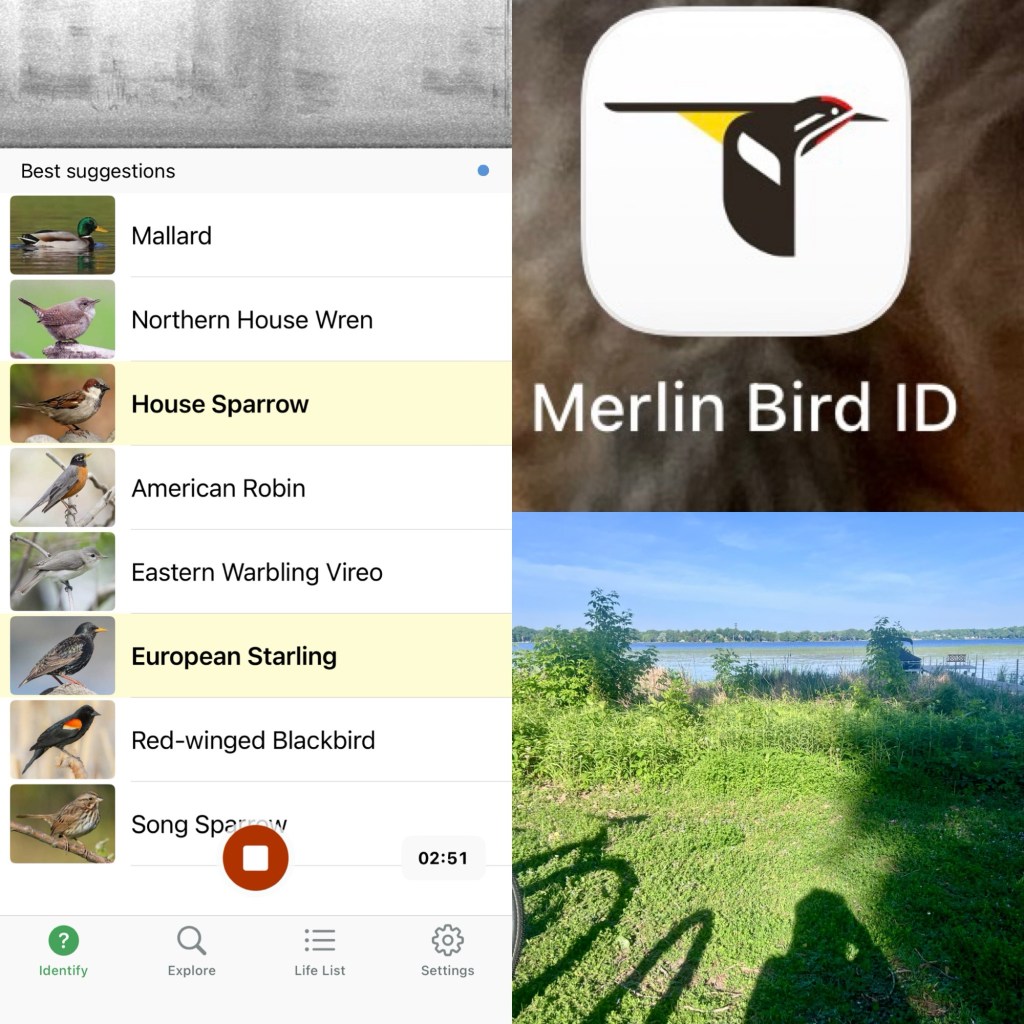

I went for an early morning bike ride around Medicine Lake this morning and stopped at a bench for a water break. The birds were in full form, tweeting their little hearts out when I remembered the app I had loaded on my phone last year.

By allowing a recording on your device Merlin Bird ID will let you know who you are hearing. The yellow band indicates a song bird in action. It’s fascinating to have access to this information, if you’re a bird watcher,

And what does it cost? The small price of keying in where you are recording from. The use of technology connects one group to another. Those collecting data about birds provide the tools. Independent birders get educated on their hobby.

Sure there are devious no-gooders, but there have always been crooks and criminals. Let crime stoppers round them up,

Meanwhile look for a group that will amplify the good in your life for a small fee or inconvenience. And get busy.

She gives most dangerous sight

To keep his life awake:

A sword sharp-edged and bright

That darkness must not break,

Not ever for her sake.

With it he sees, deep-hidden,

The sullen other blade

To every eye forbidden,

That half her life has made,

And until now obeyed.

Now he will know his part:

Tougher than bone or wood,

To clasp on that barbed heart

That once shed its own blood

In its own solitude.

I’ve enjoyed this book by George Will. It’s been an education for the mind, and a challenge for one that is missing many pieces (thank goodness for ai!) .

Here’s a bit.

There is, however, something more, something exceptional about American patriotism, something complex and demanding because it involves assent to a creed that says rights are natural to, meaning inherent in, our humanity. A rights-centered society, must, however, take seriously the fact that duties are not natural. They must be taught. Self-interest is common and steady; virtue is rare and unpredictable. A society devoted to guaranteeing a broad scope for self-interested behavior must be leavened by virtue. So measures must be taken to make virtue less rare and more predictable. Among those measures, Americans have always considered education crucial.

I feel like there has been a neglect of the sense of duty. Sometimes shockingly so. I’m not sure if it is due to the decline of jobs with implied duties of service. Or if it is fashionable for those who were once revered for service work, to now want tangible income.

How to feather duties into ones course of life more readily occurs with role models. And then once individuals feel the reward of watching a flourishing, hopefully it will self-ignite in a virtuous cycle.

I know tombstones are out of fashion, but there’s something sacred about standing at a gravesite. In that moment, we pay tribute to those who came before us—the parents, grandparents, and ancestors whose lives shaped our own. We lay flowers, say a prayer, or simply pause in silence

Or you can use the excuse of a visit to bring you back to your ancestral country, even if you’re thousands of miles from where your roots first took hold. The headstones tell stories of immigration, hardship, and resilience. The soil of your lineage lies beneath your feet.

The ritual of the visit itself is grounding. Cleaning the marker, pulling weeds, sitting on a nearby bench—these small acts become a meditation. Gravesites are peaceful places, often surrounded by ancient relics of stone and weathered bronze that have stood watch for decades or centuries. The wind moves through the trees, a light rain falls, birds call overhead, and for a brief time, the noise of the modern world fades.

It’s a beautiful form of communing with the past while staying firmly in the present. You carry their memory forward in your daily life, your choices.

We all share this truth: We live. We die. It’s the one universal experience that binds every human who has ever walked this earth. Yet in our modern world, with community activities on a smaller scale, funerals are no longer the regular communal events they once were. That makes these intentional visits to memorials even more importance.

So if you haven’t lately, consider making the trip.

Different gifts, different services. We aren’t equal in our skills. And that’s the way it’s meant to be.

Over six thousand guests watch a graduating class of 869 walk the stage for their diplomas. It is one of the largest classes in St Olaf’s history.

What separates Europe’s rise from China’s long stagnation? A fascinating answer comes from economic historian Joel Mokyr in a recent presentation.

Mokyr highlights a profound institutional divergence over the last millennium. In China, extended families, lineages, and clans grew increasingly central to social organization. In Europe, their importance declined, gradually replaced by what Avner Greif called “corporations” — associations of unrelated people who voluntarily come together to pursue a shared objective.

This isn’t just about family size. Decades of work in anthropology and psychology show that growing up in tight-knit extended kin networks shapes culture and psychology differently than growing up in societies where non-kin institutions dominate. The result is a contrast between more communitarian orientations (strong loyalty to a close in-group, weaker trust toward outsiders) and more universalist orientations (greater willingness to cooperate with strangers on the basis of shared goals or rules).

Mokyr gives concrete examples of these European “corporations”: guilds, monasteries, universities, and even military companies. Some were largely non-profit in orientation; others blended public spirit with pay. What united them was that membership was voluntary and exit was possible — unlike family, which you cannot leave.

How does this connect to real economic life?

At home-economic, we share much of this framework: most public goods are actually local or club goods, cooperation depends on group boundaries, and associational life often involves significant unpaid or underpaid contributions.

Is it possible that there is another angle to the core distinction that is slightly different?

Instead of a sharp divide between “family” versus “non-family” institutions, we observe that every transaction contains a blend of public-spiritedness and private interest. The key variable is the anchor of the interaction:

• In tight kin or clan settings, the anchor is often the family/group itself.

• In associational settings (guilds, fire departments, churches, professional networks), the anchor is usually a shared objective or cause.