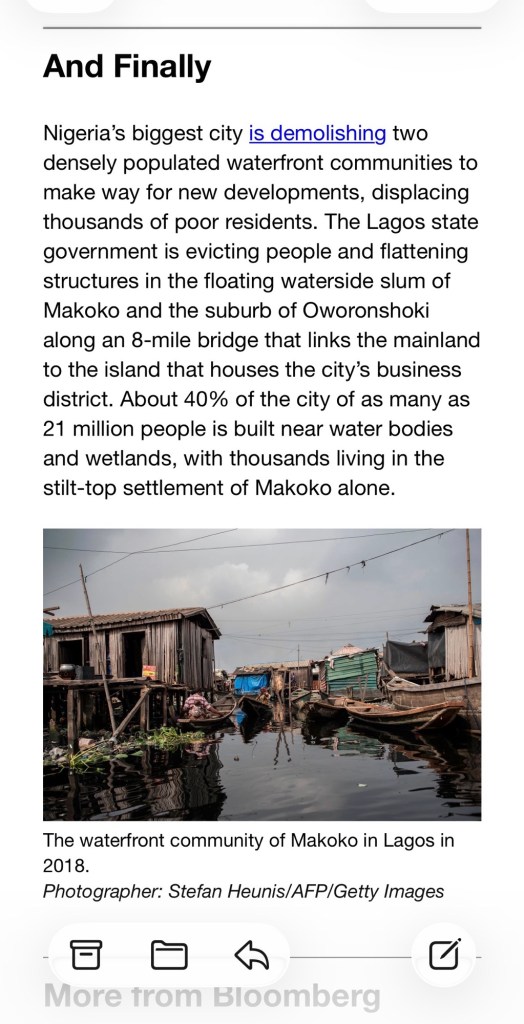

The screenshot below, from a Bloomberg newsletter, tells a story that has been told before. An area in a downtown, or alongside a river, or in a first-tier suburb, becomes blighted beyond repair. As a result, a new development is scheduled to replace it.

The question is not whether it should happen. It simply does. Over again, worldwide, across all types of geography. When the plot of land becomes more valuable for a new purpose, the natural progression is for it to be redeveloped.

On a small scale, you see it in a neighborhood when one home has been let go to the point that it does not command a price above the lot value. A new owner, or a builder, secures it, razes the structure and builds anew. At least that is what most of the neighbors desire. A dilapidated home is no fun to drive by every day. Once one property becomes blighted, it seems that others follow suit. So new is nice.

The news gets a hold of the story when a significant portion of residents are caught in this cycle, and it requires a large swath of land to turn over. That’s the story posted above. PBS covered a renovation of a large apartment complex in Richfield, The Crossroads at Penn, due to the significant number of residents were low-income.

And that’s really what the outrage is about. It’s not about renovations. It’s not about a few people who in the end are better off in a new environment for all the reasons others move: proximity to medical facilities or jobs, families, better schools, and so on. The story becomes news when the sheer number of residents involved requires more social capital than is readily at hand.

Property maintenance is expensive and ongoing. Policies that hamper repairs will yield negative returns at multiple levels. Ideally, caring for the poor entails preservation of suitable property, not its destruction.

People speculate why young people have delayed home purchases. Only around 20% of home purchases fall in this category. A historic low. But is it that surprising? Look at the surge of foreclosures in ’07-’08 and ’09. Hundreds of thousands of people who were never meant to have financial struggles lost their homes.

Children ages 8-12, old enough to sense the stresses within their families, yet too young to analyze the impact of a national financial crisis, were bystanders to these unpleasant legal actions in the early 2000’s. These are today’s young home buyers. Uncertain of what a real estate purchase will do for them. The anxiety associated with foreclosures has often been portrayed in litterature.

In Death of a Salesman, the family’s fear of losing their home emerges gradually, revealed not through a dramatic announcement but through Linda’s quiet confession that they are barely keeping up with the mortgage. She tells Biff and Happy that Willy has been borrowing money just to make the house payments—a disclosure that reframes the entire domestic landscape. What had seemed like an ordinary family home is suddenly understood as something fragile, held together by secrecy and strain.

The looming threat of foreclosure exposes the play’s deepest emotional fractures. The mortgage becomes a symbol of Willy’s unraveling identity—his failure as a provider and his desperate clinging to the American Dream. Linda’s hushed explanations carry a mournful tenderness, showing how fear and loyalty tangle together under financial pressure. For Willy, the house is both sanctuary and burden, and the possibility of losing it turns that symbol of pride into a reminder of collapse. The family’s anxiety over the home’s instability reveals how economic pressure corrodes affection, pride, and hope, tightening around them until it shapes every gesture they make toward one another.

The comparison of home prices to buyers’ incomes is a popular measure for assessing the health of the real estate market. Presently, that multiple seems high, and people are using it to cry, crisis! But is this true?

Amy Nixon posts on Twitter (now known as X):

All of economics is supply and demand.

The median household to median income argument makes sense only in an economy where we have built enough housing units per capita, and every housing unit is being allocated as a family shelter unit because it serves no other economic utility

The model breaks down when you have wealthy families buying 3-4 spare vacation homes. And mom and pop landlords hanging onto starter homes when they upsize. And institutions buying millions of single family homes. And single people living alone in two units instead of coupling to buy one unit. And foreign citizens buying homes. And people buying and using 2 million single family homes as hotels (Airbnbs)

So long as single family residential housing is viewed as and can be used as an investment or luxury item beyond owner-occupied shelter and we don’t build enough homes to offset all those other uses, the ratio pictured in the infographic below can (and will) go even higher over time

It’s not 1985. And it’s never going to be 1985 again.

What Amy says is that there is a mix of home-ownership types. If you are analyzing Lake Country, with many second homes, there will be a different price-to-income figure than if you consider a first-tier suburb built almost exclusively of starter homes. I like to call them platters. It’s the local eco-systems of properties that have interesting numbers. Averaging just smudges out all the details.

I’ll also note the shift in demographic mix. The number of first-time buyers is at an all-time low. From NAR:

WASHINGTON (November 4, 2025) – The share of first-time home buyers dropped to a record low of 21%, while the typical age of first-time buyers climbed to an all-time high of 40 years, according to the National Association of REALTORS®’ 2025 Profile of Home Buyers and Sellers. This annual survey of recent home buyers and sellers covers transactions between July 2024 and June 2025 and offers industry professionals, consumers, and policymakers detailed insights into homebuying and selling behavior.

Repeat buyers enter the market with equity. They do not need to take on as much debt relative to their income as first-time buyers do. Yet the sales price is the measure from which payment is extrapolated, not the actual payment. As a market rises, so does the equity, pushing this fictitious measure of debt load out of whack with reality.

There is no blob of “government” money, or “policy” that can make something affordable for one without making something else less affordable for another.

So if tenants get immediate relief from a rent freeze, where does that money come from?

Those outside the business may think that this will trigger a direct transfer from a wealthy landowner. Structurally this is an impractical notion. Even for those who have equity, it is just that: wealth tied up in the value of the property. It is not cash that can circulate and pay bills.

But in most all cases, the funds that come in from rent are pegged to go out to another obligation. This might be property taxes which are known to increase every year. This might be to a bank that financed the purchase of the property. And the insurance company which provides property isurance as required. This might be to a utility company. Each of these obligations have recourse for non-payment which ultimately leads to their making first claims on the income.

The funds which subsidize the rent freeze are most likely to come from monies intended for repairs and maintenance of the property. These vary from tasks that are good to do but not urgent, to things that if defrayed cause additional costs, to things that need immediate attention like a leaky pipe or a furnace outage. To give an idea of the number of routine items involved in the care of real estate, consider this post.

Over time, two things tend to occur. First, the new landlords with all their positive energy and desires to get ahead can’t maintain a financial foothold and leave. Other longer term owners prioritizes the most important fixes but let the cosemetic upgrades go. Over time more and more of the longer term components age, yards get overgrown, appliances become run down. The housing stock deteriorates.

The neighborhood at large is depreciated by blight, taking a little chunk of equity from every property owner nearby.

The biggest losers of rent control are the young, the mobile, the ambitious, immigrants, and people without a lot of cash. If you want to move from Fresno to take a job in San Francisco and move up, and you don’t have millions lying around to buy, you need rentals. Rent control means they are not available. Income inequality, opportunity, equity, all get worse.

In this paragraph, John Cochrane begins to draw lines around groups of people who will lose out under a rent-control, a policy that favors those who have established leases with landlords.

The reader can quickly imagine a young person being squeezed out of houisng by the combination of entry-level pay and bulked-up rent. The surcharge is necessary to balance out the rent-controled units. That’s the persona that comes to mind and it is the one the author intends to convey. But wait. What about the just-out-of-school coders and engineers that are swooped up by the tech companies?

These kids are paid a lot money. They are can choose where to live without much concern as, most often, they have no other attachments. They all live together in some big tech hub, often times leaving their childhood communties behind. They no longer have other points of reference like a brother who took up plumbing, or grandparents on fixed income. Not only do the have the cash flow to spend they are not being reminded that others do not.

One descriptor is not enough to form a group. To say the population of Minnesota has remained constant is light on details. Susan Bower, the state demographer, explains some of the demographic breaks down in Eden Prairie, a SW suburb of the Twin Cities. At the presentation she notes the the state loses 5,000-10,000 people a year but it is made up through international immigration. In other words, the people who leave have no concerns regarding rent control are replaced by a group who are disadvantaged by rent control.

To be efficient, matching people in consideration of their stage in life with their housing needs is best. Policies which keep people in place or discourages them from moving up, moving closer to employment, moving to a stronger school district, moving closer to support systems and so on are detrimental.

The Grumpy Economist has another great post, this time about rent control. For those of us in real estate, it’s an irritating topic. The errors in the use of price controls are numerous. Using John Cochrane’s article as a road map might be interesting to illustrate this point. Let’s start with this paragraph.

Sure, “sharply rising rents and utility bills wreak havoc on family budgets,” if the families don’t follow the screaming market signal to move. (Which is not painless, for sure. Incentives never are.) But the money comes from somewhere. Rent controls and energy price caps wreak havoc on landlord end electric utility budgets. The money must come from somewhere.

The claim is that rents are rising sharply. The reader pictures a Scrooge-like figure pounding on the door of a cowering family of four, announcing a ‘sharp’ rent increase (extra dollar symbols for emphasis), while behind this embodiment of the typical landlord stands an eviction notice ready to be served. I’d love to see numbers to this effect. I challenge that the ‘sharp’ rent increases are occurring at lease renewals.

Large corporate landlords might have a set policy of annual increases, but they account for only 3-4% of proprietors. Landlords must juggle the cost-benefit of increasing rent. As 80% own and manage the units, they calculate the costs, time, and uncertainty of a new tenant. This is weighed against a 3% increase on $1,100 or $33/mo in additional income. Needless to say, many landlords will forego a rent increase to keep a good tenant.

These subtleties are lost in real estate analysis, where all the numbers are averaged as if there were one typical renter, one typical landlord, and one typical property. This couldn’t be further from the truth. There are whole economies of renter groups. There are students who will have negative income before they join the workforce; there are singles with high-fluting jobs and no other responsibilities; there are single parents; there are couples with kids in a city just for a bit; there are elderly on fixed income with low mobility; there are recently divorcees looking for a glamorous downtown lifestyle.

Are all these groups to receive the same treatment? The same concern for their monthly budgets?Rent controls are initiated at the city level. Every group of renters would receive the benefit of a market-restrained obligation. Is that the intention?

Landlords are also assumed to be a certain type. The persona has tremendous equity in their property, no debt, and other cash they are stashing like squirrels do with acorns in the fall. And certainly some landlords fit this description. But more likely than not, the landlord has a mortgage and obligations against their time. The new entrants to the field, those trying to get ahead by getting a foothold in real estate, are undoubtedly the ones who need to make the cash flow.

When property taxes, utilities, or the cost of hiring labor rise, a landlord has no way to respond until a lease comes up for renewal. Rent control tightens this squeeze, leaving property owners caught between increasing public demands funded through taxation and their limited ability to recover those costs through rent. The first to be pushed out are often the newcomers—the small, aspiring owners who bring fresh energy and ambition to the market, but lack the cushion to absorb sustained losses.

Lesson number one. Averaging is a mistake. Assuming there is only one type of each actor in this economic trade of money for lodging makes for an impossible conversation.

There aren’t many. There’s the ‘how to get rich in real estate’ type of literature, which is only vaguely helpful to those with no real estate experience and, in equal measure, misleading. There are books developed to help salespersons pass the required testing to obtain a real estate license. There’s material on all sorts of financial instruments used to finance property. But I’m not talking about that type of thing.

I’m talking about the manner in which real estate features in people’s lives.

Judith Martin, a former professor of geography at the University of Minnesota, wrote Past Choices/Present Landscapes: The Impact of Urban Renewal on the Twin Cities. This project spotlights some of the effects I like to talk about. It focuses on the massive slum-clearing and subsequent redevelopment of large sections of inner-city property. In hind site Martin points out:

Much has been written about the ideas and the implementation of the urban renewal program in the United States during the 1950s and 1960s. Most of this literature views urban renewal as a program that: (1) worked to the disadvantage of people most in need of improved housing -a great deal of substandard housing was removed, but a relatively small amount of low-income housing was constructed;(2) was a boondoggle for developers-they were able to acquire land inexpensively from city authorities, and often made large profits on the projects built on this publicly acquired land; and (3) focused on economic development issues C’let’s fix up downtown”) at the expense of housing and neighborhood concerns (Anderson 1964; Hartman 1964; Gans 1965).

Viewed in retrospect, much of this criticism is valid, but it does not tell the whole story. Critics have portrayed planners who developed and implemented urban renewal programs as heartless beasts who turned a deaf ear to the real needs of “the people.” But it is hard to see most renewal officials as greedy and profiteering, or as consciously trying to exercise their power over helpless city residents. There are, for example, no notable cases of renewal officials growing rich working on these programs. If anything, the views of those who implemented urban renewal programs in the Twin Cities and elsewhere can be considered somewhat naive. They assumed that renewal could be accomplished quickly, that private developers would clamor for the opportunity to build in available areas, and that the renewal process could be carried out with relatively few snags. None of these assumptions proved to be true.

Real estate is a tricky wicket. If people want to follow along, they need to, as Judith indicates, read the whole landscape and not cherry-pick a brief situation in the misty flow of time.

There continue to be mobile home parks across the metro offering one of the most affordable form of housing. The structure is considered a vehicle and licensed as such. The home is anchored on a lot in a mobile home park and rent is due every month in a similar fashion to association dues. People like to talk about tiny homes now. Still, manufactured homes can be reasonably constructed in a factory and meet the same quality and amenities as RV’s, another acceptable form of shelter.

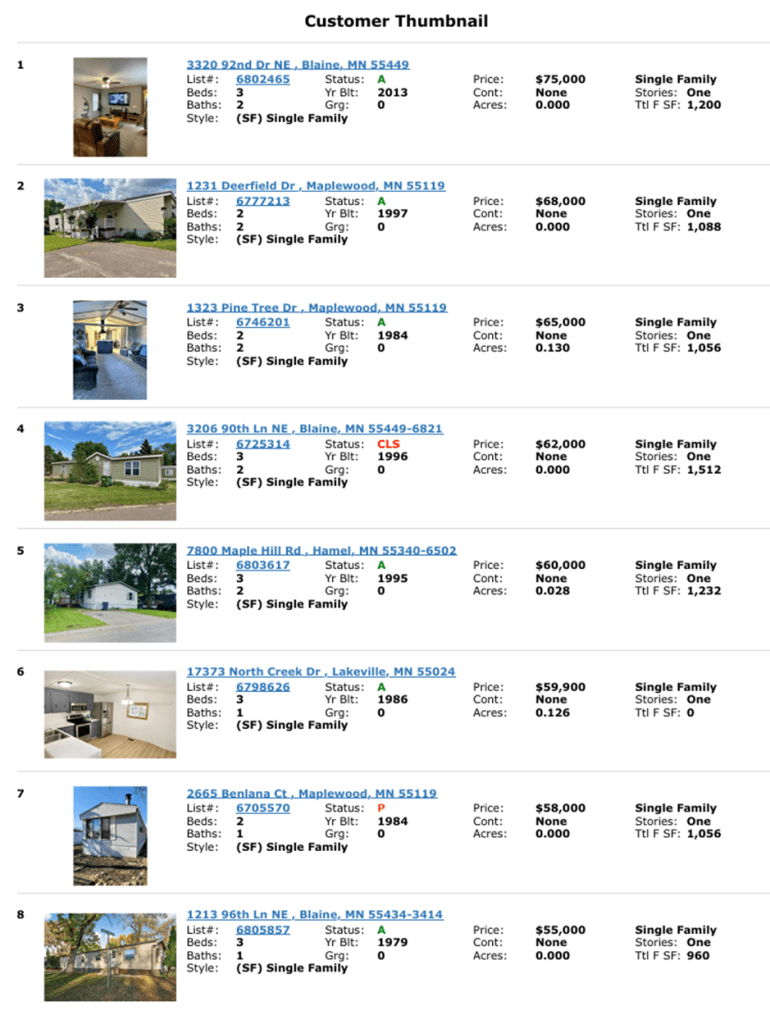

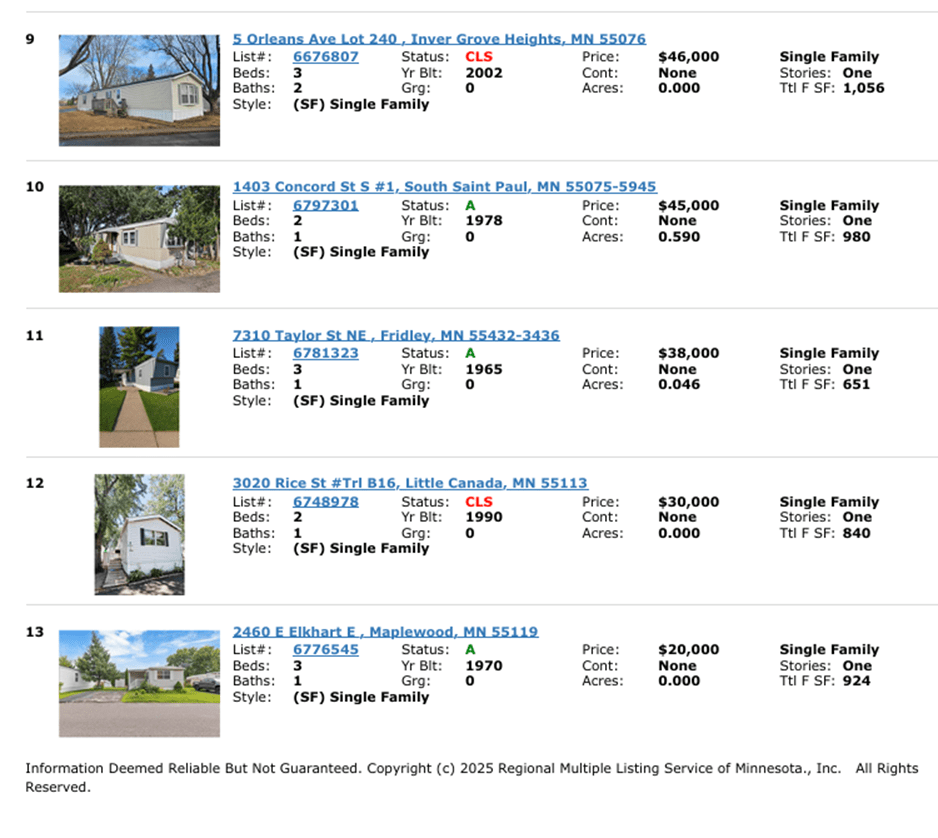

:Here are some current listings and recent sales:

Few mobile home parks rise to the level of civic engagement that can be seen in Landfall Terrace, a community on the eastern side of the metro. As with many good things it starts with its history.

James and Mitzi Olson used to own all of the land in Landfall. They moved here in 1953 into a cottage that was hardly better than a log cabin. …The Olsons had lived in a mobile home during World War ll and knew that there was a shortage of affordable housing, so they developed their site into a mobile home park. As it was on the early highway between St. Paul and Hudson, Landfall developed several businesses, including a truck stop, restaurant and nursery, most of which left when Interstate 94 was put through and access became limited.

Often successful things are born out of a basic need of local people. But it is only through nurturing and ongoing maintenance that group projects survive. Especially one a s successful as this.

Landfall is a city in Washington County, Minnesota, United States. The population was 843 at the 2020 census and it is the smallest community in Washington County in terms of area. It lies on the eastern shore of Tanner’s Lake on Interstate 94.

Landfall is an incorporation of a manufactured home community, contributing to its reputation as the most affordable community in the Twin Cities. In 2008 & 2010, the city was named one of the 100 best communities for young people by America’s Promise.

Landfall is one of only two incorporated cities in America that consist primarily of manufactured housing.

I showed a house this week in a modest but well-situated neighborhood. It had some problems, but mostly superficial– carpet, paint, appliances, and the like. Yet, even at a price below the comparable sales, it remains on the market. What? Uncertainty.

The property has been through a foreclosure, and as the tax records show, the bank holding the paper, Midfirst Bank, repurchased it. But this is a murky ownership situation.

At a sheriff’s sale, the buyer is not immediately given a full and clear ownership title the way they would in a normal real estate closing. Instead, the buyer typically receives one of two legal instruments depending on the state:

Sheriff’s Certificate of Sale (common in states like Minnesota)

This document shows that the buyer purchased the property at the sheriff’s sale.

It is not a deed and does not yet transfer full title.

The original owner still has a redemption period (often 6–12 months, depending on the type of property and state law) to pay off the debt and reclaim the property.

Sheriff’s Deed

If the redemption period expires without the former owner redeeming the property, the sheriff’s certificate is converted into a sheriff’s deed (sometimes automatically, sometimes requiring a filing).

The sheriff’s deed conveys whatever interest the debtor had in the property to the buyer, but it usually comes without warranties of clear title. That means the buyer takes the property subject to existing liens, unpaid taxes, or other encumbrances, unless state law says otherwise.

The property is being marketed by the owner who went through foreclosure, even though their right to the property is only through redemption. They would have to find a buyer to settle the full amount owed to Midfirst. This middle-ground ownership area makes the market uneasy. What if the bank wants more than the sheriff’s sale for fees and expenses? What if the property’s condition deteriorates between the offer and closing? Who will handle the repair? Will the title transfer be handled properly in the end?

Minnesota’s foreclosure rate is very low at one-half of one percent of the housing stock. So these sales are rare, and an investor will undoubtedly find it worthwhile to take on as a project. But in areas with insecure property rights and poor banking relations, the surcharge for uncertainty carries a hefty surcharge.

Housing markets often seem mysterious, but at their core they operate as a cascading system shaped by wealth, supply, and lending rules. A recent model by Abramson and Landvoigt highlights how rising wealth inequality and slow housing supply interact to push prices upward. Their framework divides housing into quality tiers, from luxury to starter units, and shows how households with different levels of wealth compete across these tiers.

A central insight is that prices at the very top do not stay isolated. Luxury buyers are a small share of the market, and in some sense they simply bid against one another for exclusivity. One might argue that they are “fools” for paying such large premiums, while the rest of the market should remain relatively affordable. But in practice the tiers are linked. When supply of luxury units is restricted, affluent households who cannot find space at the top tier shift down into the next-best homes. That displacement triggers a chain reaction: middle-income households face stiffer competition, prices at their tier rise, and the pressure filters all the way down to lower-income renters. Economists call this the filtering or musical chairs effect, and it means that adding supply at the high end can improve affordability across the board.

This cascading dynamic is exactly what makes the market work. New supply at any tier frees up units that can be occupied by someone else, allowing households to sort themselves according to means and preferences. The danger arises when either end of the ladder is blocked. If new high-end supply is not built, the wealthy bid down-market and crowd out others. If older or more affordable stock is neglected, the bottom rungs collapse and low-income households are left without viable options.

At the same time, credit standards shape who can actually buy. A household that cannot afford the payments will not receive a loan, which protects individuals from becoming dangerously over-leveraged. But this underwriting filter does not stop prices from rising overall; it only determines who gets excluded. The clearing price is still set by those wealthier households who can obtain financing. Those priced out of ownership often remain in the rental sector, where demand pressures drive rents upward as well.

Taken together, the picture is less about a simple split between the rich and poor and more about a tightly connected cascade. Housing affordability depends not only on overall supply but also on how well each rung of the ladder is maintained and allowed to expand.

I flew into Missoula today and the Montana Airport is wrapping up a major multi-phase expansion that reshapes regional travel and brings broader economic shifts in its wake. Here are some of the details:

The Physical Build-Out

Total Cost: Over $110 million for the full terminal expansion.

What’s New: New gates, expanded baggage claim, rental car lanes, security upgrades, and room for new routes and carriers.

Who’s Paying: a combo of the Feds and private interests

Federal: More than $50 million in grants, mostly from the Bipartisan Infrastructure Law.

State & Local: Matched funds from the Missoula Economic Partnership, businesses, and banks—no local tax dollars used.

Recent Boost: A $6M federal grant (2024) will help complete the next terminal phase.

Skyward Travel Growth

Missoula set a passenger record in 2024: Over 1 million flyers, up nearly 12% from the year before.

Targeting 1.5 million by 2044 as travel demand soars.

Now offering more frequent flights and year-round service to Chicago, thanks to an $875k federal grant.

The Ripple Effects

📚 University of Montana Perks

Easier access = stronger recruitment, research partnerships, and conference travel.

Out-of-state students now find Missoula more reachable and appealing.

🏘️ Housing Pressures

Expansion is fueling demand for housing, especially near the university and airport.

Rent hikes are real: Locals report steep increases, with “affordable” now starting near $1600/month.

Development impact fees (passed on to buyers) may also be contributing to rising costs.

💼 Local Economy

Jobs during construction and in airport operations.

Tourism boost: More flights mean more visitors spending at hotels, restaurants, and shops.

Stronger air links help regional business and health access.

🚧 Challenges Ahead

Affordability squeeze: Residents and students are feeling the pinch from rising rents.

Infrastructure stress: More travelers and new residents will test city roads, utilities, and services.

Equity concerns: Growth must be balanced to include long-term residents and low-income communities.

Final Approach

Missoula’s airport expansion is more than a construction project — it’s a gateway to growth. With smart federal funding and local vision, the region is positioning itself for a more connected future. But keeping Missoula livable as it grows will take coordination on housing, transportation, and community needs. How would one go about making some projections? Estimates of impacts and time frames could be interesting to local public leaders.

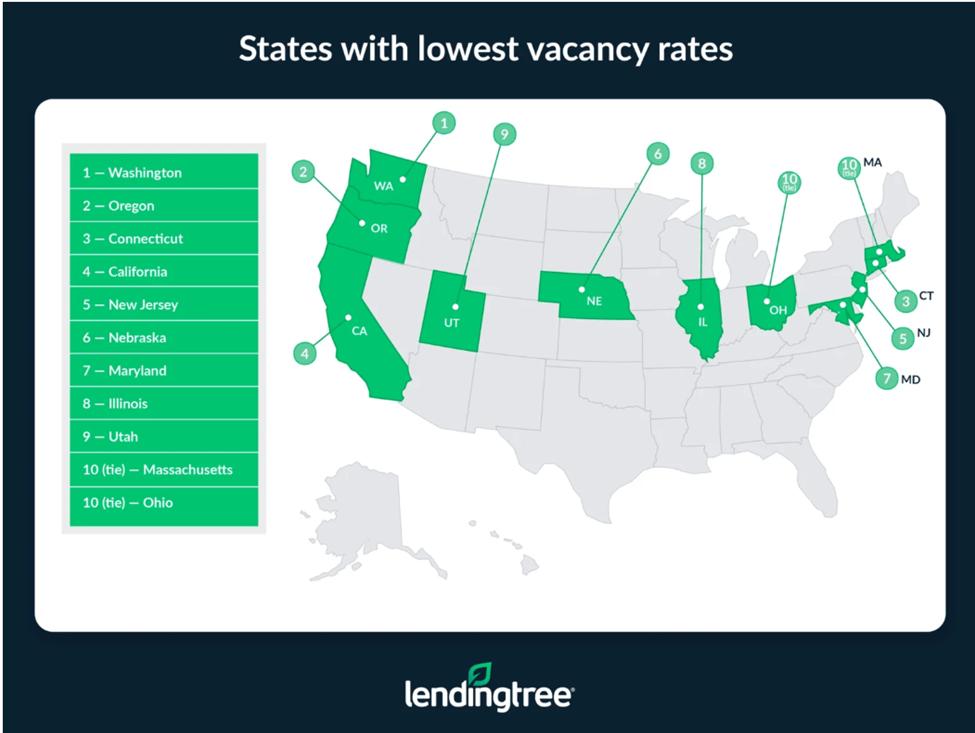

Some claim a housing crisis is underway, but I’m not so sure. If the pressure for homes were severe, one would expect most properties to be occupied, leaving others stranded without a place to go. Vacancy rates provide us with additional information. An article by LendingTree, 14.9 Million Homes Are Vacant in the US — Here Are the States With the Highest Vacancy Rates, provides a great overview of the topic.

Vacancy rates differ significantly depending on where you look in the country. If you’re looking at Maine, you’ll find the highest vacancy rate in the country — 21.09% (157,467 vacant homes), according to our analysis of the U.S. Census Bureau 2023 American Community Survey (ACS) with five-year estimates. Following Maine at the top is Vermont, with a 20.06% vacancy rate (67,606 vacant homes), and Alaska, with an 18.24% vacancy rate (59,745 vacant homes).

Together, these three states account for nearly 285,000 vacant homes — out of 14.9 million vacant homes nationwide.

Nationally, the vacancy rate is much lower than that of these three states, with the U.S. average sitting at 10.43% — a figure that translates into nearly 15 million vacant homes. While that may sound like a lot, it may not feel like it if you’re searching for a place to live. That’s because not all of those properties are available to rent or buy.

In addition to seasonal and vacation homes, others are classified as vacant because they’re in transition — those that are rented but not occupied and sold but not occupied. Homes for migrant workers, which they occupy during crop season, are also classified as vacant.

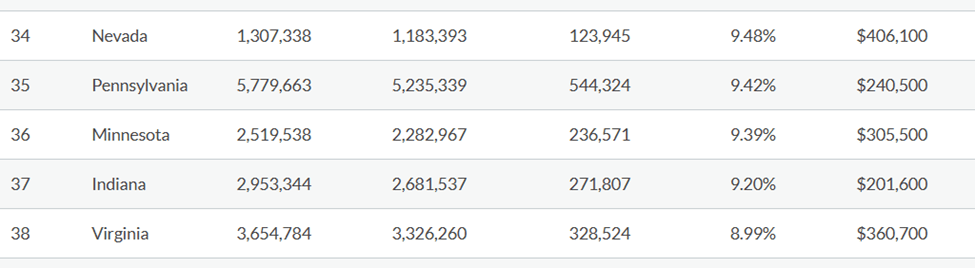

Minnesota, as is often the case, is just average. There are 236,571 homes vacant, which, in percentage terms, is 9.39%

The article cites a list of reasons why a home could be vacant. It might be a second home or vacation property. It might be in a transition state from either a remodel or a relocation of residents. Sometimes people hang onto properties for emotional reasons, such as a family tie to the land.

But note, in any case, that there is a variation between the states. Real estate is local. National generalizations about the state of housing are often dumbed down and not particularly helpful.

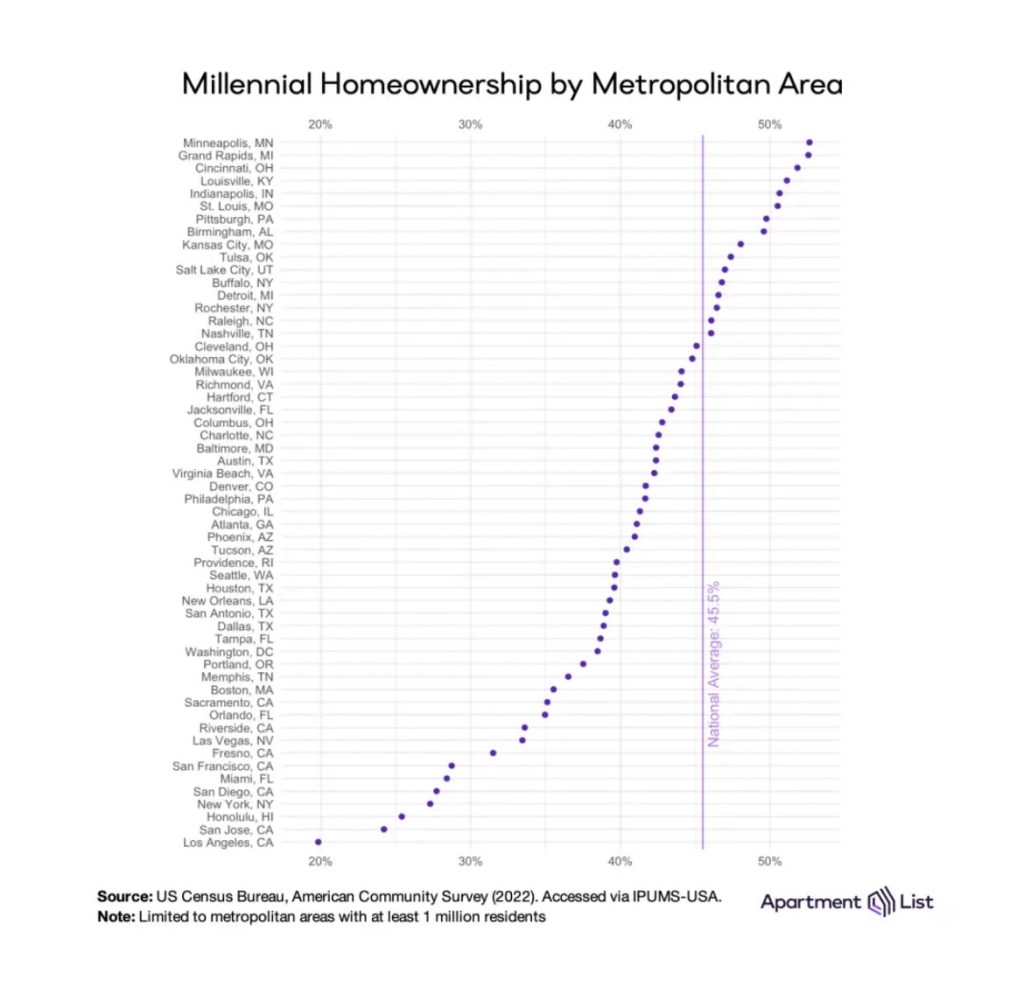

Lists are fun, especially when your team is ranked at the top of the list. In this case, Apartment List pulled data from the Census to show that homeownership is the highest amongst Millennials in our area. Over 50 percent of folks in the 29-44 age range choose to own their homes rather than rent them.

Many will say that this is about price, as residents in San Jose and LA —cities at the bottom of the list —don’t own homes due to the high prices. And that’s a broad stroke, likely to be true, observation. But the list is long, and there are many other cities between the two extremes. So what else makes for a culture of ownership?

I’ve worked with some first-time buyers who don’t end up buying, and this is what seems to play on their minds. They are afraid they will lose the house in foreclosure. Someone close to them, perhaps even more than one, lost a home to creditors, and the negative experience frightens them. Second, they are afraid they will buy a lemon. Homes are complex, comprising many components. It’s easy to feel overwhelmed with the responsibility of keeping it all running smoothly. Lastly, they are afraid of adversarial neighbors.

Here’s a further breakdown of homeownership rates amongst all age groups in Minnesota.

I speculate that the last group has a homeownership rate of 77% because of the following factors. Low foreclosure rates keep the negative and traumatic experience of losing a home out of people’s lives. Since many residents grew up in owner-occupied households and experienced the ups and downs of repairs throughout their lives. They also have these folks in their lives to turn to for guidance. If the buyer has lived locally for most of their lives, they gravitate toward areas where they find the family and friends.

Minnesota rarely experiences the dramatic price swings that are more frequent in the coastal states. Hence, real estate tends to be a stable and reliable source of equity. People buy for pride of ownership and independence as well as frugality.

I thought the US Census was a factual thing. It is meant to report data, not succumb to opinion. This headline, however, which is being used nationwide as a rally call against housing markets, is a product of capture.

The census people want us to believe that nearly half of renters are in financial straits.

How did they get this number, and why does it seem high when you look around in your life and don’t see that half of the people you know or come into contact with are shouldering the pressure of a cost-burdened housing expense? The threshold used to determine financial distress occurs when a household spends more than 30 percent of its income on housing expenses. It is said that this is an industry norm– meaning lenders of all stripes rely on this benchmark when determining creditworthiness.

That’s not to say that lenders do not approve borrowers with a higher debt-to-income level. They do. In fact, they will lend up to 50% in situational circumstances. Note that up to these levels, the financial institution is still anticipating that the loan will be repaid. Delinquencies are not the objective in the lending business. (Here’s a post on debt-to-income ratios from a few days ago.)

But that’s not what this headline implies. According to the census, 30-50% of the population is ‘burdened.’ Perhaps one could let that go to semantics. Only the ratio calculated in this case differs from the industry norm. This ratio includes utilities as a monthly expense, where the industry standard does not. So, how does the added cost of heating bills, electricity, water, and possibly internet (I’m not sure what the American Community Survey includes) adjust the threshold and push a larger share of the population over the 30% threshold?

The first thing to know is how a debt-to-income ratio is calculated. Take an average rental cost of $1300 a month. The monthly income amount for a 30% debt-to-income ratio is $4333/mo. If you add $139 in utility costs, everyone adjusts up 3%. An added monthly cost of $200 (say the respondent includes all their streaming options), then the debt-to-income ratio rounds up another cohort by 5%. It’s safe to say that the census is no longer using an industry standard by calculating ratios with additional monthly obligations.

Is the renter who likes streaming services cost-burdened or simply choosing an entertainment option? Is the renter who elects to pay a larger portion for rent to live on a metro line, forgo the cost of a car payment, and net out a lower monthly expense as a result, cost-burdened? Is the renter who selects a living option close enough to an ex-spouse to share custody and not pay child support cost burdened or cost savvy?

People arrange their monthly budgets all the time with savings and benefits that may not be readily apparent to the outside world. That’s the beauty of choice. As long as a market is loose enough for people to navigate to their best circumstances, they arrive at a combination that works in their best interest, reflecting all facets of their lives.

College students will undoubtedly pay more for rent than their income would seem to allow. That’s the reality of their stage of life. Seniors also fall into a different category of consumer than working adults. Many could be at a stage where their monthly living expenses may include food and care, while their monthly income may just be one source in their retirement plan for covering expenses at the end of life. Are these students octogenarians, cost-burdened, or simply living their lives as planned?

Affordability is a subjective measure. I question the Census’s objectives in publishing opinions on affordability in the housing markets. What’s next? Will we be told we can’t afford to take a vacation or to take the summer off to be with our kids? Or should the Census return to the way it was– a fact provider?

In a paper entitled Property Rights Paradigm, Armen Alchian suggests ownership is more intertwined than one might think.

There is some ambiguity in the notion of state or private ownership of a resource, because the bundle of property rights associated with a resource is divisible. There can and does exist much confusion about whether a resource or “property” is state or privately owned. Some rights to some uses of the resource may be state owned and others privately owned. While it is true that the degree of private control is increased when additional rights of use become privately owned, it is somewhat arbitrary to pass judgment on when the conversion to private control can be said to change the ownership of the bundle of rights from public to private. The classification of owners can be carried beyond the important state and private dichotomy. Corporate, school, and church owners of property are also of interest. The structure of rights can have important consequences for the allocation of resources, some of which we now illustrate.

Think of the home you own. The deed at the county recorder’s office says you own it. But the utility company may access the property if it needs to do a repair. The city workers can drive a skid steer into your lot, dig a big hole to check the city water connection, without checking whether you have a graduation party planned for the weekend. Of course, the county can tax you for local services, and if you fail to pay, they can take your property.

So you own your home more in unison with the public than you might have thought.

What about going the other way? Do people pay more for property if it has better access to taxation-supported services? It makes sense that they would. Public groups may have formal or informal claims against your home. There’s a good chance these were sought after when they decided to move. A portion of the price acts as a place maker for value– or in other words, the market prices institutions, too.

In a recent paper co-written with researchers from the University of Wisconsin-Madison and the University of Illinois-Chicago and initially published by the Minneapolis Fed, we measured the evolution of housing quality for low-income households over the past several decades across the United States. We found broad and generally large increases in housing quality and smaller but still important increases in living space.

So, it’s not surprising that the data show fewer low-income people living in squalor.

I like this part too. It’s a great example of how headlines can suggest misleading information. Although gross rents have increase, they have hit people’s monthly budgets at a much lower increase.

As housing quality and quantity are getting better, how much more are households paying for it? According to the AHS, for below-median-income Twin Cities area residents, real monthly spending on housing increased by 32 percent from 1998 to 2021, from $1,008 to $1,333. Around half of below-median-income Twin Cities households remain housing-cost-burdened (spending 30 percent or more of their income on housing) and a quarter remain severely housing-cost-burdened (spending 50 percent or more of their income on housing). For many families that spend a large fraction of their income on housing, findings about general housing improvements may be tough to appreciate.

However, our analysis indicates that greater housing spending reflects not only higher housing prices but also Twin Cities area residents’ ability to afford housing that is larger and nicer. Overall, the average housing budget share only increased by 4 percentage points from 1998 to 2021, from 36 percent to 40 percent of income, which indicates that most of the growth in spending on housing is driven by higher incomes, better quality, and more spacious homes, as opposed to needing to allocate a greater share of income for the same, unimproved housing.

Some combination of private money, public efforts, and community involvement is improving living standards for those with lower incomes. And it’s not clear at all that the burden is falling on the most vulnerable.

At least a couple of decades ago, when I’d help a client purchase a home that happened to be along an open field, I’d remind them that the view may not always stay that way. The Twin City metro was growing and fields just like the one adjoining their new home were being plowed in and repurposed into neighborhoods of single-family homes. They would nod in acknowledgement and yet still feel a loss when a crop of dwellings soldiered up outside their windows.

There are more situations like that– where the surrounding circumstances change and present residents feel like a cost is imposed on them. Take that lightning rod word: gentrification. In certain circles, it is spit out with as much vehemence as the title capitalist. In reality, gentrification implies that a neighborhood is getting cleaned up, crime is being brought down, structures are being fixed up, and truancy is being pushed out. But when you spruce up the place, more people want to live there. This is distressing to longtime residents who don’t want to see rent prices rise in response to higher demand. The situation is changing around them without their consent!

Or consider an elderly couple who own a large, beautifully situated parcel of land on Flathead Lake. In the years they moved to northwestern Montana, it was remote. Desolate even. Over time, others discovered their paradise and passed the word along to still more people who appreciate views of the rugged snow-capped Rockies. As people arrive, more services are necessary which pushes up property taxes. Is it fair for the elderly to endure the increases? They did nothing to give rise to these new obligations, and now the expense may make their living choice beyond their reach.

Tariffs are a response to the same issue. When the pool of labor is opened up to a global market, should the loss of work in the Midwest manufacturing industries fall solely to die-cutters and assemblymen? They did nothing to change the circumstances, yet they bear the burden. Wall Street profits, labor abroad profits, and they are told to adapt.

What is the proper cycle of protection for the renter affected by gentrification? How long would the elderly be eligible for lower property taxes? Is there a natural circuit for these things to enable an easing of the effects of changing circumstances to all involved?

Kevin Drum proposed that in a 2022 article– and I agree entirely.

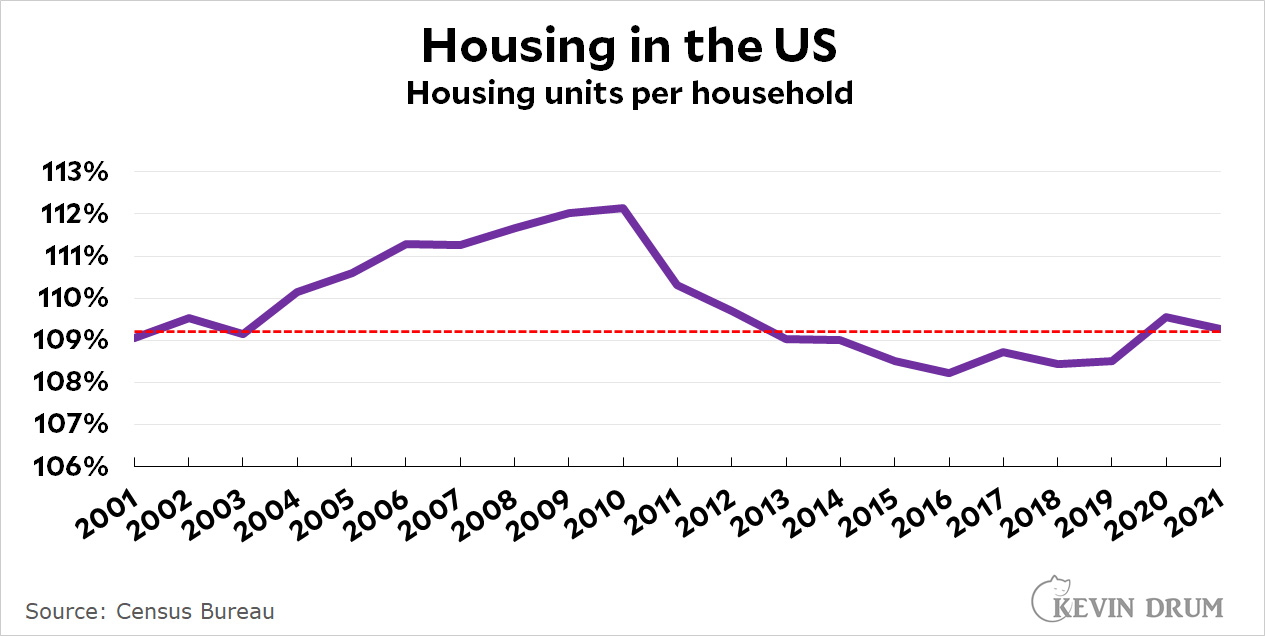

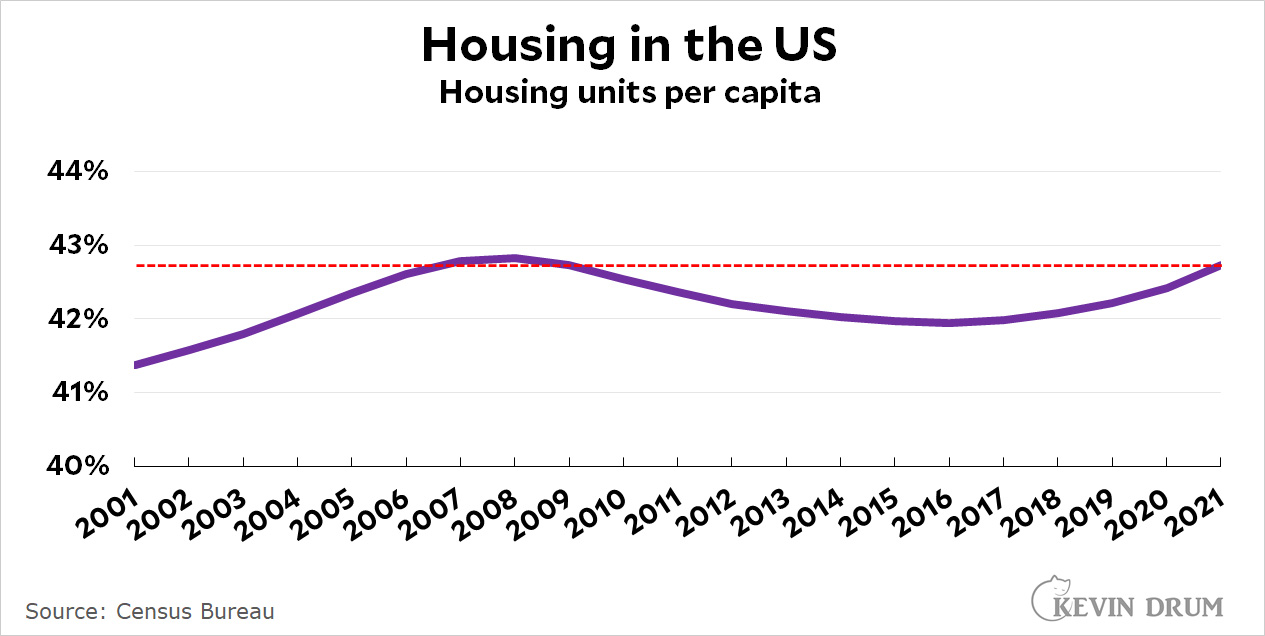

The real issue here is that America doesn’t have a housing crisis.

I’m not sure why, but I find the new urbanists one of the most annoying groups in the progressive pantheon. It’s not because they’re wrong, precisely, or because they’re meanspirited, or anything like that. There’s just a disconnect from reality that seems to motivate so much of what they say and do.

Take America’s housing crisis. Here it is:

We have as much housing per household as we had in 2001. And just in case you think I’m cheating with this “household” business, here it is per person:

We have more housing per capita than we did in 2001.

Just wait and see as the market softens. Prices in some markets have already ebbed away from a peak, and the number of homes on the market is creeping up. Builders who notoriously hold on to their list prices are marking spec homes down a bit. The tight market was not due to a shortage as much as the normal pressure of people moving to changes in their lives.

But the best part of Drum’s article is how he feels about the people who try to set a national agenda on housing: the urbanists.

But this still doesn’t really explain why I find the urbanists annoying. Here’s my real beef: they are obsessed with big cities. They spend nearly all their time trying to convince us that big, crowded cities should become even bigger and more crowded. Or that suburbs should become big and crowded, just like cities. This is a fantastic waste of time. Residents of big cities don’t want to become more crowded and resident of suburbs don’t want to become more like cities. They will fight you forever on this. Absolutely forever. The game isn’t worth the candle, especially when there are so many other far more useful things we could be devoting our energy to.

So why waste time on this? The urbanists will haul out studies about economic gains, environmental impacts, mass transit, etc., but they massively oversell those benefits and completely ignore the downsides of crowding. Instead, they should be spending approximately 100% of their time promoting policies that would get people out of big cities and into smaller cities that have room to grow.

It is funny how everyone wants to talk about ‘world-class cities.’ Ho-hum cities are where it is at for understanding the baselines of success.

CNN brings readers up to date on the antitrust lawsuit against the National Association of Realtors. The plaintiffs were granted $418 million last summer, not a small amount of cash. Once all the legal bills were paid, the 500 petitioners received an estimated $900.

So, did all that work and expense result in a new way of doing business?

“Paperwork has changed, and I think some really good things have happened in the way most of us discuss commissions upfront with our buyers and sellers,” said Brita Kleingartner, a Realtor in Los Angeles. “But I don’t think that business has changed in any way.”

With mortgage rates hovering around 7% for the last six months and average home prices across the US continuing to rise, the new rules, which took effect in August, had spurred hope that commissions paid to real estate professionals would plunge, making homebuying and selling less expensive for average Americans. Last year, TD Cowen Insights estimated that the new rules could cause fees paid to Realtors to fall by 25% to 50%.

Instead, commissions have remained largely unchanged since August, according to a study released this month by real estate platform Redfin. For relatively lower-priced homes that sold for under $500,000, Redfin found that the average commission has increased since the rules took effect.

As I predicted a year ago, how business is done has not changed. The lawsuit alleged a problem that did and does not exist. How do we know? Watch the consumers and what they do. If they choose not to employ two realtors (one to represent the seller and one to represent the buyer), if they decide to pay them at a different rate, then their pull in the market generates a change. If consumers, despite all the layer’s fees, publicity, and exposure, continue to desire representation by a professional licensed agent, then the market rate is being met in an open and non-coercive environment.

Is all this activism worth it? I wish someone would keep track. A legal battle of this size is expensive. Plus, the plaintiffs who were encouraged to participate spent valuable time on this versus other aspects of their lives. It tapped into some of their family capacity for civic participation. Could other causes within their immediate circles better deserve their efforts? Very possibly.

Many feel a moral superiority by fighting the good fight. But when the fight goes to show that the monsters were but mist off a lake on a cold fall morning, then one must count up the expense of it all and do an analysis.

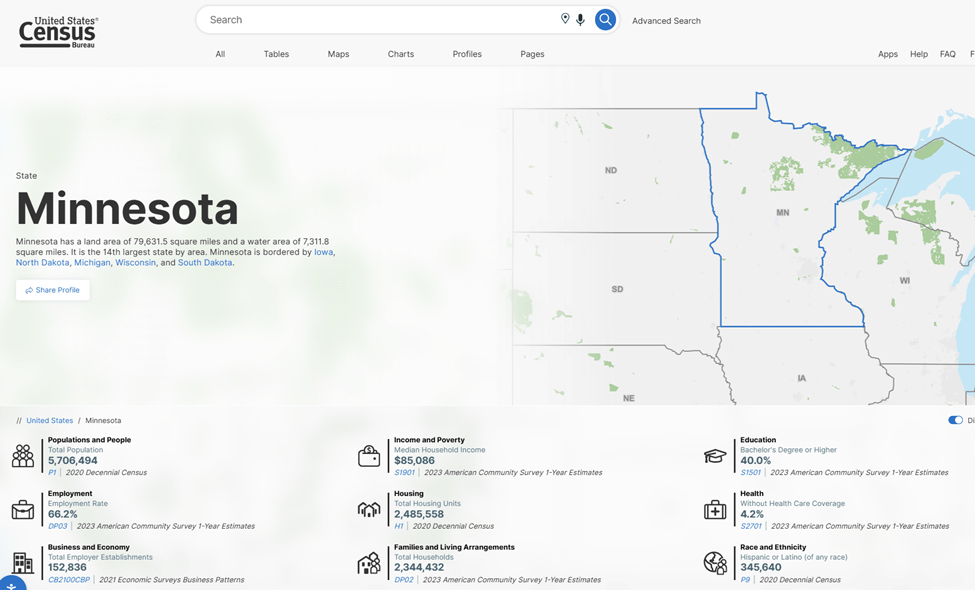

The US Census has a new look. The site has improved tremendously. This might be old news, but it’s news to me. It’s worth checking out if you haven’t been there in a while. I particularly like the profile pages, like this one.

Take note of the breakdown of housing units and households. There are approximately 5.7% more housing units than households in the state. You need some vacancies as there are units under renovation or being held while a family relocates from one living situation to another. Is 5.7% in the comfortable range? It’s hard to know. Still– comparing the spread between households and units is a measure to determine how many extra spaces, if any, there are for families to live.

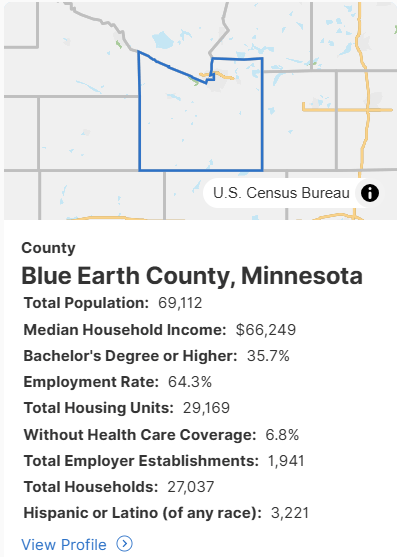

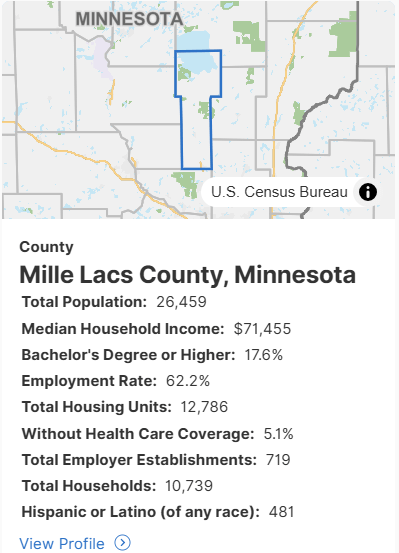

The county-level profiles are great too and come in several formats. Here are three to compare.

Each county has a different spread between the number of housing units and the number of households. The range is from 7% vacancy in the agricultural area of Blue Earth to a low of 1.8% in the most densely populated Hennepin County to a generous 16% in the northern lakes area of Mille Lacs County. Hennepin County is the only place we can say with certainty that there is a clear need for more housing.

Counties are large. There may be vacant structures in rural Blue Earth county while the demand for places to live is in Mankato, a nice-sized town of forty-five thousand. For that reason, it’s great that the Census even zooms into the city level.

Here’s a snapshot of Perham, a small but humming town about an hour SE of Fargo.

The point here is that housing is local. When people observe that the price of housing did not come down when new units were added, the follow-up question should be, what type of housing and where?

In a recent post, House Prices and Quality: 1971 vs. 2023, Jeremy Horpedahl points out the difference in house prices by time values, which I really like for comparison purposes. He notes, “As you can see, in 2023 it took 31 percent more hours of work to buy a square foot of the median home, compared with 1971.” Furthermore, he makes the adjustments for the extra footage most homes offer today versus when the Brady Bunch lived in their swanky multi-level Californian home.

Then he goes on to say the quality of construction in the 1970s was modern and hence met a certain threshold of acceptability. I would argue that’s not the case. The 70s was a time of experimentation with new methods driven by a desire to enhance eco-friendliness. These materials and techniques did not provide the same longevity of use as the old country techniques from earlier in the century. This article cites a variety of issues. Focusing on a few mechanical components of a home will best exemplify how the norms and standards of the time affect the durability of the product, which is internalized in price.

Homes are expensive to buy and to maintain. One justification for paying the premium for new construction is that all major mechanicals are warranted for ten years, and most, on average, will last more than that. Heating and cooling systems have an average lifespan of fifteen years and cost $12-14K. Roofs keep homeowners dry for twenty-two years or so ($15K). Windows and siding can vary significantly depending on the quality of the materials.

For instance, in the photo on the right, the windows are original to the 1912 apartment building. They are wooden double-hung sashes that protected the lower level laundry and storage area from the weather for a century, serving the purpose intended. The windows on the left are vinyl replacement windows that were installed less than fifteen years ago. The dirty-looking glass is called a broken seal. Moisture has found its way through the double-paned structure, dictating that they are a failed mechanical by industry standards.

Window repair and replacement are among the more costly repairs in a home. The insert on the left probably costs about $3,500 in our market, just for one window.

The 1970s were full of experimentation with lower-quality materials. Hardwood flooring was replaced with plywood and then covered with carpet. Whereas wood floors are sanded and refinished for a beautiful crisp feel once every twenty years, carpet wears out in about a third of the time, seven years. My hardwood flooring guy tells me they have been back to refinish quarter-inch oak in one-hundred-year-old homes. There is the esthetic appeal to this home feature but it also translates to lower upkeep.

Solid stucco exteriors (stucco is a cement-like product that lasts for thirty years or more) are another application prevalent in homes built prior to the 1970s. Exteriors were instead clad in inexpensive plywood. This fibrous product does not necessarily fail in functionality after twenty years but no longer takes paint well and hence looks thrifty. Woodpeckers tend to find it appealing for sharpening their beaks as well.

By the late 1980s, homes built in the 1970s were highly unpopular. In part, their split entry style and vaulting with dark beamed ceilings had lost their cosmetic appeal to younger buyers. Buyers also longed for quality craftsmanship. The seventies homes were built cheaply, and consumers felt it. Most people wouldn’t have verbalized their selection as a commentary on an experiment in housing gone wrong, but they showed it in their choices.

Crisis [ˈkrīsəs], noun, a time of intense difficulty, trouble, or danger.

Let’s consider a few housing facts to see if the state of our housing needs rise to that level in MN:

According to the US Census, Minnesota’s homeownership rate has hovered between 72% and 76% in the last four years. This is well above the national homeownership rate of 65%.

Minnesota’s foreclosure rate is down 9% from last year and ranks 27th nationwide with 370 homes in foreclosure or 1 out of 6,740. (Attomdata)

It seems that many Minnesotans can afford to own homes. Few are having difficulty maintaining their ownership positions. Crisis of homeownership averted in the far north.

That’s not to say that there may be housing issues for non-homeowners. Princeton University tracks evictions. Minnesota is third from the bottom on their list, at 4%. So renters don’t seem abnormally stressed or in crisis.

For those undergoing foreclosure or eviction, there is a crisis. Thus, they should receive the appropriate support to help them navigate their way to a solution to reestablishing shelter.

There is a crisis. It’s a crisis of wasteful regulation. So, call that out and make efforts for reform where needed.

Allison Shertzer takes issue with the headline’s cryptic economic message. If there is enough housing, then the price for occupancy should settle to the price each resident can afford. If there are fifty homes in a settlement and fifty households, then those who can pay the most pick first, and down the line, the pricing match shuffles until the last match of the least desirable to the household to those with the least resources. This simplified balance market omits nuances like how two homes are tied up when people transition from one property to another. Or that when major renovations are underway, it is difficult to live on the property, so it is vacant.

The basic premise, however, is that when there are sufficient structures to shelter every household, the price to live in those structures is pushed through the system to reflect consumers’ ability to pay. After all, even at the lowest end of the scale, it would be better for the property owner to receive some income from a less advantaged person than to let the property sit vacant.

Or is it?

It is refreshing to see a study confirming that dwellings are, in the big picture, available in sufficient numbers. “The numbers showed that from 2010 to 2020, household formation did exceed the number of homes available. However, there was a large surplus of housing produced in the previous decade. In fact, from 2000 to 2020, housing production exceeded the growth of households by 3.3 million units. The surplus from 2000 to 2010 more than offset the shortages from 2010 to 2020.”

This article tries more than most to zero in on what is concerning. It’s not affordability in general. When ten parties are bidding on a house, that tells us there are plenty of households who find the price within their range of acceptability. When houses are selling, and apartments are rented, then folks have the funds to make those arrangements work.

What is of concern, and has always been of concern, is sheltering those at the very lowest of means. This brings us back to the question: If there are open units to occupy, is there a reason why they would be left vacant instead of settling for some cash flow? Yes, there is a reason. In some cases, the net monthly cash flow is negative. The issue is being talked about as if it concerns the building, but it’s really about the necessity of support services.

It would be even more refreshing if the conversation went in that direction instead of hammering away about building affordable housing, which is another cryptic economic fallacy.

Consider the stylized fact that unmet demand is most-inexpensively delivered on low-cost land at the periphery of the commuting shed, known as a “greenfield” site. This type of development uses low-cost, low-density construction methods. However, in productive and desirable urban areas, low-cost land—especially close to jobs and retail—is quickly consumed, pushing single-family home builders farther away from the amenities that make these urban areas attractive. Eventually, this progression reaches a limit in which commuting back to these amenities is too costly. At this point, the greenfield land is effectively “built out,” and developers are forced to look inward to more expensive land closer to the core where spatial amenities are valued by renters and buyers. When this “infill” development becomes a larger share of new housing supply, the marginal cost of supplying a new housing unit will increase, and the elasticity of supply will fall. Thus, even in the absence of different regulatory regimes, an MSA with more population and more density will appear to have a steeper supply curve because large and growing urban markets naturally progress in this direction.

Real estate has a history of being talked about in static numbers. Orlando and Redfearn discover a dynamic in their research. A city grows along the fringe where the developers can build over large parcels of undeveloped land. This is the most consumer-friendly by meeting the desired structure for the lowest cost. But at some point, the authors observe that the commute to a central business district causes infill projects to gain in status. At that point, a city gains new units within the old infrastructure instead of in the greenfield.

Much of what we have learned in the two decades since DiPasquale (1999) first prompted the field to investigate housing supply is aggregate and static in nature. The goal of this empirical work is to document the location of housing stocks within several MSAs over a long time of growth. The results presented in the article are largely descriptive. It is abundantly clear that aggregate analyses miss the compelling dynamics we documented.

Why stop at the trade-off between low cost fringe housing versus commute time? There are many other interesting dynamics to expore.

In this five minute video clip, Frederick Melo with the St. Paul Pioneer Press refers to a number of important real estate outcomes. He was invited to the weekly PBS show, Almanac, due to a recent announcement that a portfolio of commercial buildings, including the iconic First National Bank Building, is being listed for sale.

The collection of buildings are owned Madison Equities. Long time real estate developer, Jim Crockarell died in January and his heirs are not interested in being landlords. Building owners can gain emotional attachment to their properties as appears to be the case here. Some of them were half empty and some completely empty. Significant vacancies do not happen on the turn of a dime. Commercial leases are multi-year and companies have an investmest in their locations. So this recent announcement reflects activity which has been brewing for a while.

Well known architectural firm, TKDA, is also moving. They are relocating to Bloomington to keep workers happy. After 100 years, the downtown devotees are succumbing to practical desires for free parking. An added feature is scenic vistas over the Minnesota River. To attract workers back into the built environment, they are seeking out new surroundings in the third largest city in the state.

US Bank is also stepping away from downtown yet still staying in St. Paul. Workers here also say no to the densest part of the city. Melo reports that the building has had ghost leases for years. While technically under contract, the one-employee-per-floor occupancy has been a long-time indicator of what the future held.

What to do with all these vancant buildings is the question of the day. The solution under proposal is converting the office space to living space. But conversions are very expensive and the demand for residential in the capital city is not as strong as next door neighbor in her sister city. It’s a tough place to live.

Grants and tax increment financing are being proposed as public interventions. Is this a good idea? I’m not so sure. The mayor is quiet letting a non-profit alliance offer investment strategies. Their approach is to focus on one street at a time. One street a downtown does not make.

Cathy Wurzer brings in the ringer of a topic just at the end. Crime and personal safety. These are real issues that have been muted in the last four years. People don’t want to have to worry about being carjacked at knife-point when they’ve got a head full of kid’s programming and an armful of work manuals. Proximity to violence is a deal breaker for many people.

I had not heard of the study the Downtown Alliance had done around the DT Greeters pre and post pandemic. Within a district where a tax was collected to support the greeter program, quality of life crimes decreased by 40%. Whereas in the adjacent Lowertown area (where the St. Paul Saints stadium is located) crimes increased by 20%. Jim Crockarell, the real estate developer, opposed the district. This is speculation, but I’m guessing he thought greeting people and being busy maintainers of sidewalk safety was meant to be organic. It was the civic thing to do. Yet here is concrete data that an organized effort to deter crime, a significant motivator, was successful with subsidized labor.

In review, we were told about multiple exits to the city core. Be careful to note this was not a sudden occurance. We heard about emotional attachments beyond the pull of financial prudence. We heard about consumer driven needs for parking and easy access. We heard about the impracticality of retrofitting the built environment (file under why so many old buildings come down). We heard about public subsidies that will fall woefully short of the task. We heard about the big driver, safety, which is often kept on the QT so as not to implicate an area.

The higher interest rates have cooled the residential real estate market a bit, which is nice because for a run of three years or so, every home that was in decent condition was selling in multiple offers. It was common for a buyer to bid on four, five, seven homes before they were the winners.

Recently at a sales meeting the manager pulled the topic out of his list of things to talk about at a meeting because some properties are still attracting several offers. The strategies the office came up with filled the large sheet of paper on the easel at the front of the room. There’s more than one way to write and present an offer to a seller.

This made me think of game theory as the purpose of the meeting conversation was to theorectically compare strategies amongst the active participants in the market. Like in game theory, agents develop a sense of their buyers valuation of the home. There are many angles to this, but given the process of considering other options, perhaps loosing out on other bidding situations, the agent shares the strategies discussed amongst the agents in the meeting, and advises the buyer accordingly.

While reading Isreal Kirzner work, I thought his concept of discovery best described the process buyers go through in the market to arrive at their home purchase. After repeated investigations into the various housing options, perhaps with breaks in between to go home and reassess the purpose of the move, buyers discover their best option and only then are motivated to pursue an offer to the seller.

I can see now that the game theory part is the setup for strategy, competition and cooperation with the seller once the property has been identified. The discovery part has to do solely with the buyers insights into which property has that added benefit that boosts the property ahead of others in accomodating their needs. It is more useful to them and their particular circumstances.

It’s funny beause often a buyer is attracted to a property for the some or all of the same reasons the seller has enjoyed it during their tenure. And that affinitiy for the same likes and dislikes encourages the parties toward cooperation.

If you are buying land from an individual or a group please follow the following STEPS to avoid being CONNED.

1. Ask to see the TITLE DEED or Copy of the title deed. Then do a search at the ministry of lands to confirm who the real owners… pic.twitter.com/uLG9SLE2ly

A coalition of diverse groups, it was reported, were all coming together for a housing bill. That was sixty days ago.

(KNSI) — The Central Minnesota Builders Association is throwing its support behind a piece of legislation aimed at addressing the lack of housing and the high cost of new construction.

A coalition of housing advocates and bipartisan lawmakers joined together at the State Capitol to call for an increase in access and affordability in housing through the Minnesotans for More Homes initiative.

The bill (HF 4009/SF 3964) legalizes missing middle housing and new starter homes across Minnesota.

From the builders association to affordable housing advocates, an unlikely melange of interested parties were looking for ways to reduce housing costs. How better to lower expenses then to reduce barriers to building by rolling back the rules. This bill brought authority over what can be built where to statewide control.

Once the implications of un-zoning the neighborhood hit local communities, residents weren’t impressed. Here are some of the changes proposed.

Sets a base level for density allowed on any residential lot by right (or without needing to go through a discretionary review processes) regardless of size at 2 units statewide and 4 units in cities of the first class. If certain conditions are met, 8 units are allowed in second-, third-, and fourth-class cities and 10 units may be allowed per lot in cities of the first class.

Forces administrative approvals of projects that meet the standards in the bill language and prohibits public input in the approval process.

Limits minimum lot size requirements to no greater than 2,500 square feet for first class cities and 4,000 square feet for all other cities except for Greater Minnesota cities with populations of less than 5,000.

Requires all cities to accept Accessory Dwelling Units on all residential lots regardless of size and allows property owners to subdivide their lots by right.

Prohibits off-street parking from being required close to major transit stops and limits off-street parking minimum requirements to 1 spot per unit in other areas.

Allows multifamily buildings to be built up to 150 feet tall on any lot in a commercial zoning district.

Broadly prohibits design standards for residential development and eliminates minimum square footage and floor area ratio requirements.

The cities organized and alerted their constituents who must have followed thorugh with calls to their state representatives as the bills is no longer progressing through the chambers. I doubt constitutents will agree to handing over local property rights to the state. This seems like a heavy handed, top down approach.

So how does one encourage increased density? Why- the market of course!

Rent control is counter productive. From the Federal Reserve Bank of St. Louis:

Weighing Trade-offs

Economists generally have found that, while rent-control policies do restrict rents at more affordable rates, they can also lead to a reduction of rental stock and maintenance, thereby exacerbating affordable housing shortages. At the same time, the tenants of controlled units can benefit from lower costs and greater neighborhood stability—as long as they don’t move.4

For policymakers considering rent control, economics can help them anticipate possible effects and may even inform policy design for those who decide to pursue such policies. Given the trade-offs, policymakers must balance maintaining affordability for those with rental housing, while possibly shrinking the stock of affordable housing for others, especially when such housing is already in short supply.

Targeting a pecuniary benefit to a low-income group seems like an easy solution. The shift of funds from the property owners to a social value, however, promotes undesireable long-term social shortfalls. These include the convesion of rental property to owner occupied housing as the incentives cause landlords to exit the market. Or a deterioration in the quality of rental housing as, again over a longer time frame, long term maintenance becomes more difficult to fund.

On a trip to Manhattan a few years ago, my son and I noticed boarded-up store fronts along the best sidewalk shopping in the city. From the layers of flyers pasted on the brick wall and the thickness of dust perched on the window ledge, it was apparent that this state of disuse was a longterm thing. It didn’t make sense. What would make an owner prefer to leave a space empty instead of collecting rent from a desireable tenant looking for a desireable location?

If you were to think of this interms of a model, one might say, what are the negative implications of renting a storefront that zero out the benefit of incoming revenue from a tenant? What circumstances cause a property owner to be more interested in sitting on a vacant portion of a building rather than maximizing profit?

I say a portion of the building because the street level space of a NYC building is most always a small percentage of the entire building.

When an investor is looking to acquire new property there’s a lot of calculating to evaluate its prospects. The price of the building is mostly determined by how much cashflow the structure can generate. The lender (as in most cases there is financing involved) is also interested in the return their borrower will receive. This determines their comfort level in receiving payment on the debt.

With this in mind, a seller will often take action, prior to going on the market, to make the property attractive not only to the buyer but to all other parties involved in the transaction. For instance, an inspector will most probably make some rounds and look for mechanical flaws. The easy fixes are best done up front. Often there is a target renter in mind for the property and enhancement will be made to their structural preferences.

When a property goes for sale, there are lots of incentives to shine the place up and present it in its best light. Any salesperson will tell you this is how to generate the best offer.

Now fast forward twenty years, or thirty years, and the young investor with ambitions to build a portfolio has done exactly that. He or she is wealthy. There is a nice amount of equity in the property and the stress to recover every dollar in rent in order to pay the bank, the insurance company, the regulatory agencies and do repairs has eased. If the property is in a strong location, it is garnering a nice return year-in-year out. Often, it is better than other investments can offer.

Now, let’s consider the rental transaction for the storefront. It’s been a couple of decades since the property has had a full upgrade. Perhaps the paint is looking a little faded. Perhaps the interior tile work has more chips in the tile than some deem acceptable. A new younger set of folks want just that much more than what was available before. So for a bit more money in rent the owner is dealing with a lot more in either managing expectations or renovations. Renovations almost always means interacting with a regulatory entity as well. Once on the property, other issues may be brought to light.

There are two factors that go into the cost-benefit calculation of securing the lease. The rent received. And another important factor which we will call the engagement factor. When the owner takes on a new tenant they are agreeing to engage with their expectations, their payment and request idiosyncrasies. It’s not just the dollars. In the same way an insurance claim is not just about getting reimbursed for the repair work. You have to deal with the insurance rep, meet three contractors to get bids, and supervise the work. There’s an engagement factor. The street level activity also has an engagement factor. If the public has become more truant, than property damage or security issues create a cost on the owner’s time.

It gets to the point that the hastle of interacting with others starts to draw down the marginal benefit of the extra rent. Throw in a potential tax implication and that little benefit could shrink to almost nothing. An empty unit creates a tax write-off. A rented unit throws off income that is now taxed at higher rates, as many deductions have run their course.

The store fronts could be collecting dust because the engagement factors are simply too expensive.