How I remember the build-up to the financial crisis of the early oughts is explained well in Phil Gramm and Donald Boudreaux’s book, The Triumph of Economic Freedom.

The root cause of the financial crisis was the government policy to promote public objectives with private capital, which destroyed mortgage-lending standards. Government regulatory policy pressured banks to make bad loans and forced government-sponsored enterprises to purchase and securitize those loans. In addition, the government manipulated financial institutions’ capital standards to encourage banks to hold massive quantities of mortgage-backed securities. When the housing bubble burst and subprime loan defaults soared, the authors of the very housing policy that caused the crisis blamed capitalism and greed and, in the process, expanded the very governmental powers that caused the crisis in the first place.

The Feds were trying hard to encourage loans to disadvantaged groups in particular. People were so certain that there was ill will at hand, but thorough documentation confirmed that the low numbers were due to the inability to qualify, not social group standing. Thus, it made sense to loosen underwriting standards for everyone, at least in the moment. And not only force the lending institution to give loans that went against their better judgment, but to push loans out the door to meet community reinvestment goals. Talk about crossing spheres and ill-placed dynamics.

But it did increase homeownership across the board. At least until all those adjustable-rate mortgages push people right back to renting. Many took years to recover the courage to become homeowners again.

So yes, greed did get in the way. But not the greed, or rather not only the greed of the big money players. The self-interest of literally everyone in the chain was tugged right along in this whiplash dance to disaster—from the mortgage originators to the brokers to the title closers, and, most importantly of all, to the self-control and internal monitoring of the general public. The movie, The Big Short, does a good job of rolling this out.

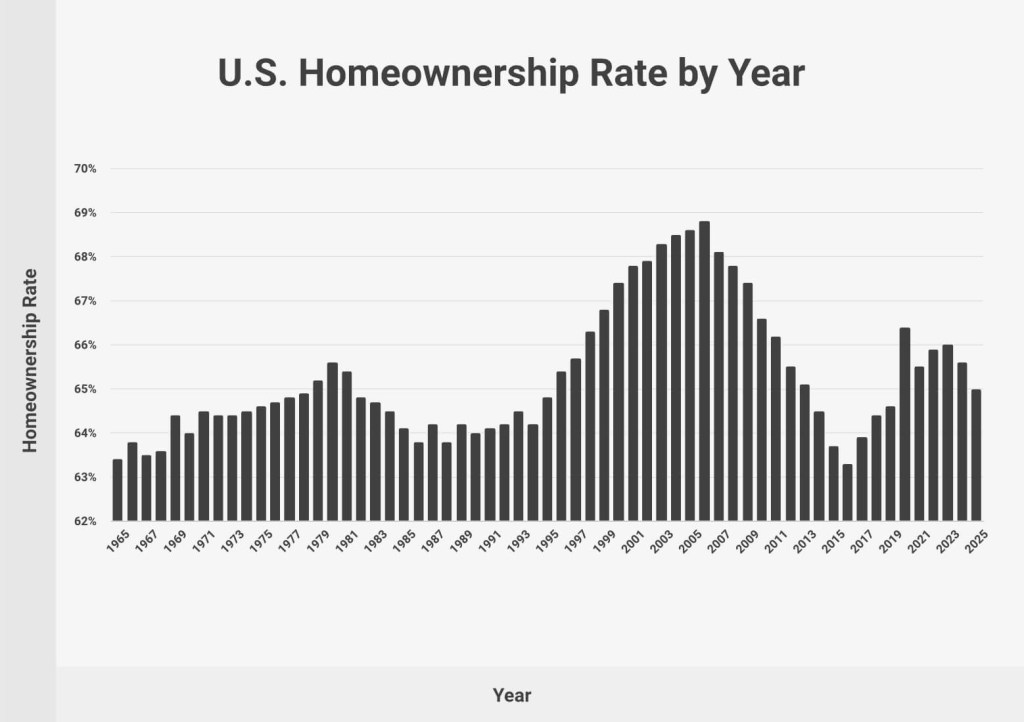

The natural rate of homeownership seems to run at about 65%. This is a global number. I’m sure there’s much more nuance to ownership rates as you group and sort households. That might be a better approach to understanding the levers to increase ownership in targeted areas.